INTRODUCTION

China has undergone an economic transformation of historic proportions. With average annual growth rate of 9.5% sustained over the last two decades, and a population of 1.3 billion, there have been major ramifications domestically, internationally and for the agricultural sector. China is now one of the world’s largest producers and consumers of agricultural products [1]. As its rapid economic expansion has allowed more and more Chinese to enter the new middle class, meat has moved from the side of the dinner plate to the center.

The beef industry is an emerging industry which is developing rapidly following policy reform and opening of trade, and it has been one of the fastest growing industries within the Chinese livestock sector. In recent years, China has been a major player in the global beef industry in terms of production, consumption and trade. On the production side, China is the third biggest beef producer in the world and is the largest in Asia [2]. Beef cattle production has been a traditional activity and an important contributor to the economic growth of China. However, rapidly increasing beef consumption per capita [3,4] has made the gap between production and consumption gradually widen. This gap is growing due to low productivity in the beef sector and a shrinking cattle inventory in China. This has led China to enter the international market as a beef consumer and resulting in it becoming one of the world’s largest beef importers [5]. With this significant increase in beef imports, China had gradually become a net importer of beef instead of net exporter.

This paper provides an overview of the Chinese beef sector, with a periodic review of changes within China beef cattle industry including beef production, consumption and trade during the period 1996 to 2015. This review also provides a brief overview of prospects for the beef industry in China.

CURRENT SITUATION FOR BEEF PRODUCTION IN CHINA

Regional distribution of beef cattle in China

As one of the most populous developing countries in the world, China has a rapidly-growing beef cattle industry that includes industrial strains and indigenous breeds of cattle (not including buffalo). Specific breeds are found more commonly in distinctly different agricultural regions of the country. These regions can be divided into three different categories according to the feed resources and environmental conditions extant in the respective regions [6], namely farming regions, pastoral regions, and farming-pastoral regions. These can be partially captured by disaggregating the beef industry within 17 provinces into five zones including Central Plains (Shandong, Henan, Hebei, and Anhui), the Northeast (Jilin, Heilongjiang, Liaoning, Inner-Mongolia, and North of Hebei), the West (Gansu, Shanxi, Niangxia, and Jinjiang), the Southwest (Sicuan, Chongqing, Yunnan, Guozhou, and Guangxi) and others.

Cattle are concentrated in the intensive cropping areas, especially in the Central Plains (Shandong and Henan) and the Northeast (Jilin and Liaoning) [7]. There are low densities of cattle in the “other” Southeastern provinces, while in the more extensive grazing systems of the Northwest large cattle herds are distributed over large distances. Beef cattle population densities in the Southwest are formed by diverse areas of intensive crop-cattle systems and grazing systems in more mountainous areas. Cattle producers in farming regions formulate diets for their cattle based mainly on crop residues and grains. Operators in pastoral regions graze cattle on pastures with only limited supplementation. Producers from farming-pastoral regions graze cattle on the grasslands during the daytime and confine cattle during the evening when they provide supplements in pens in the form of self-produced grains and crop residues.

Composition of cattle operation in China

In China, small farms are a major component of the beef cattle industry. Of the 15.5 million households that turned off 1 to 10 head per year, one-quarter exited the beef cattle production sector between 2003 and 2015 [8]. More than 90% of Chinese cattle operations slaughter nine or fewer cattle per year [8]. These operations slaughtering nine or fewer cattle yearly represent over 50% of the beef cattle industry in China. Chinese beef cattle slaughtering is mainly done by individuals, and there are less large-scale slaughtering enterprises. Beef cattle farming is mainly concentrated in agricultural areas, the amount of beef slaughtered in agricultural areas accounted for more than 2/3 of the country, mainly concentrated in Henan province, Shandong province, Hebei province and other places, and beef cattle breeding in pastoral areas are mainly concentrated in Inner Mongolia, Xinjiang and Gansu provinces. The large-scale slaughtering enterprises including Haoyue in Jilin, Kerchin in Inner-Mongolia, Qinbao in Shanxi, Benfu in Jilin and Yisai in Henan, have modern slaughtering equipment to process the beef and set up brand and chain shop to meet the middle and high-end consumers’ demand in Chinese beef market.

At the same time, many imported Australian cattle slaugh tering enterprises have an impact on the domestic beef cattle industry. In recent years, Australian beef cattle slaughter program successively started in China. In June 2016, the Australian beef cattle slaughter project started in Cixi city, Zhejiang province, and in August 2016, the imported Australian beef cattle breeding and processing project was signed between China and Australia in Rizhao, Shangdong province. Although there is less actual slaughter at present, it is expected that there will be some competition for domestic beef slaughtering and processing enterprises in the future.

Cattle inventory, slaughter head, and cattle extraction rate

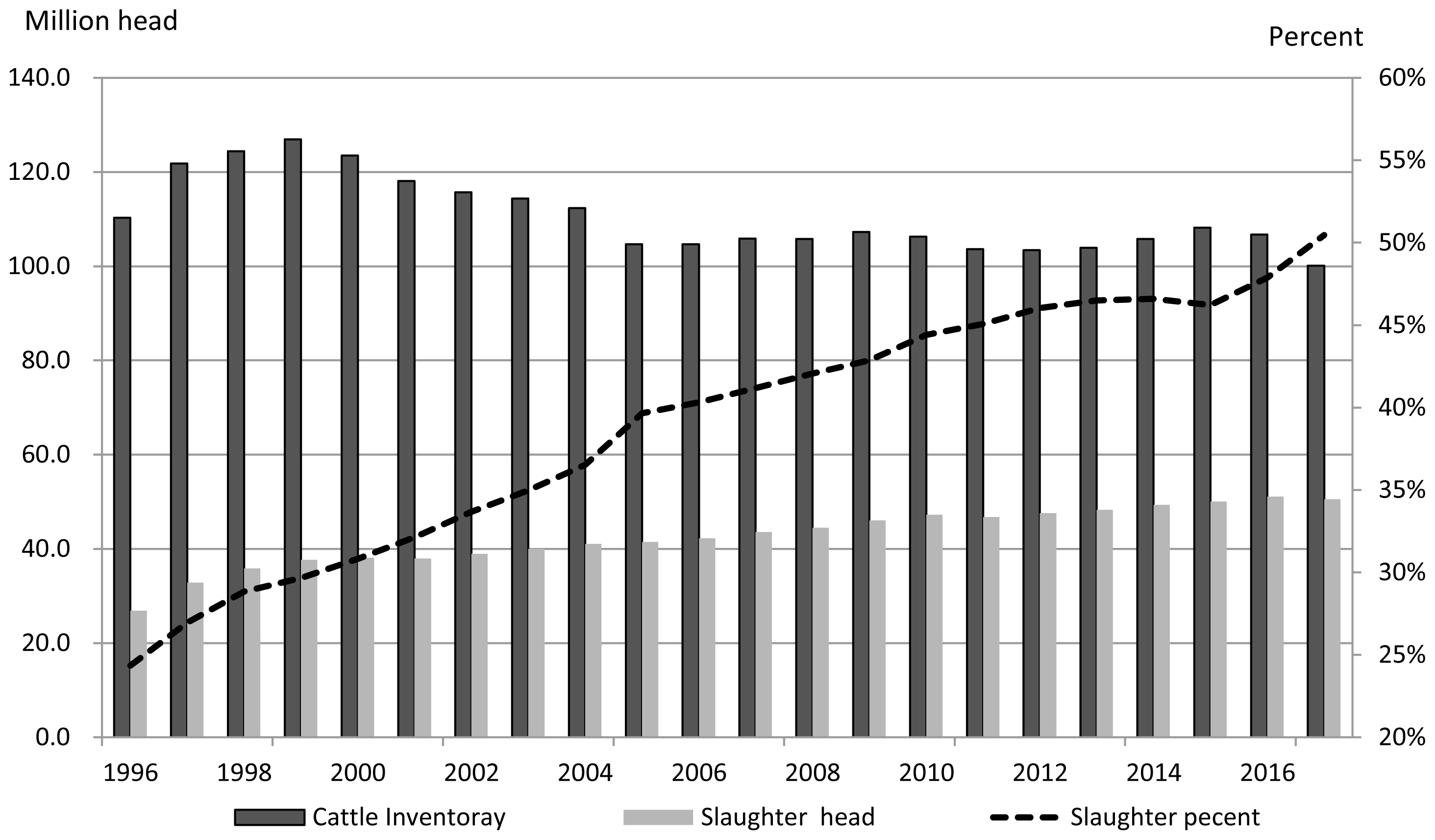

China is one of the largest cattle producing and beef consuming nations in the world. The fluctuation of the cattle inventory (including yellow cattle, buffalo, and yak) in China is shown in Figure 1. The cattle inventory experienced a sustained rise during the period 1996 to 1999. It reached a historic peak of 127 million head in 1999. During the period 1999 to 2005, there was an obvious downward trend in the cattle inventory, and the number of cattle in China decreased by 22 million head, or 21%, which may be a critical indicator for the future of the cattle industry of China. Between 2006 and 2017, the cattle inventory in China was stable at 100 to 108 million head.

China has witnessed the rapid growth of the quantity of slaughtered cattle. The number of animals slaughtered and the inventory extraction rate (slaughter head/beef cattle inventory) in China from 1996 to 2017 are also shown in Figure 1. During 1996 to 2017, the annual quantity of slaughtered beef cattle reached the historic high 50.50 million head from 26.86 million head. The extraction rate was 24.4% in 1996 and increased sharply to 50.46% in 2017. The average annual extraction rate grew by 3.6% over the period due to steady increases in total number of head slaughtered and beef consumption in China. The rapid growth mainly resulted from the sustainable growth in beef production and domestic consumption, and the booming slaughter and processing industry in the corresponding period.

Beef production in China

Total meat production in China increased by 88% between 1996 and 2016, as shown in Figure 2. This has been accompanied by a considerable increase in the production of pork, beef, poultry, and mutton. The output of beef increased 2.7% per year from 3.56 million tons in 1996 to 7.17 million tons in 2016, an increase of 97% over the past 20 years. The percentage of beef contributing to total meat production was 7.8% in 1996. In 2007 the percentage had increased to 8.9% which is the peak level in recent years. From 2008 to 2014, the percentage of beef contributing to total meat production has declined to below 8%, although increased slightly to 8.12% in 2015.

Cattle inventory in China dropped by about 8.5 million head or 8.1% between 2004 and 2013 (Figure 1), while beef cattle slaughtered and beef production have increased, as shown in Figures 1 and 2. As a result, China’s cattle industry has entered a vicious cycle in which high demand for beef has resulted in increased slaughter of females, causing cattle herds to shrink. The shrinkage in the national cattle herd has reduced the production capacity of the Chinese cattle industry.

In 2017, the beef cattle industry in China entered a transi tion period, and the beef output is generally stable. According to report of National Beef Cattle Industrial Technology System, the domestic slaughter of beef cattle was about 20 million tons in 2017, the total production of carcasses was about 5.78 million tons, and the net meat output is about 5.01 million tons. However, beef production in China won’t grow rapidly due to the long period of beef cattle breeding.

Beef consumption in China

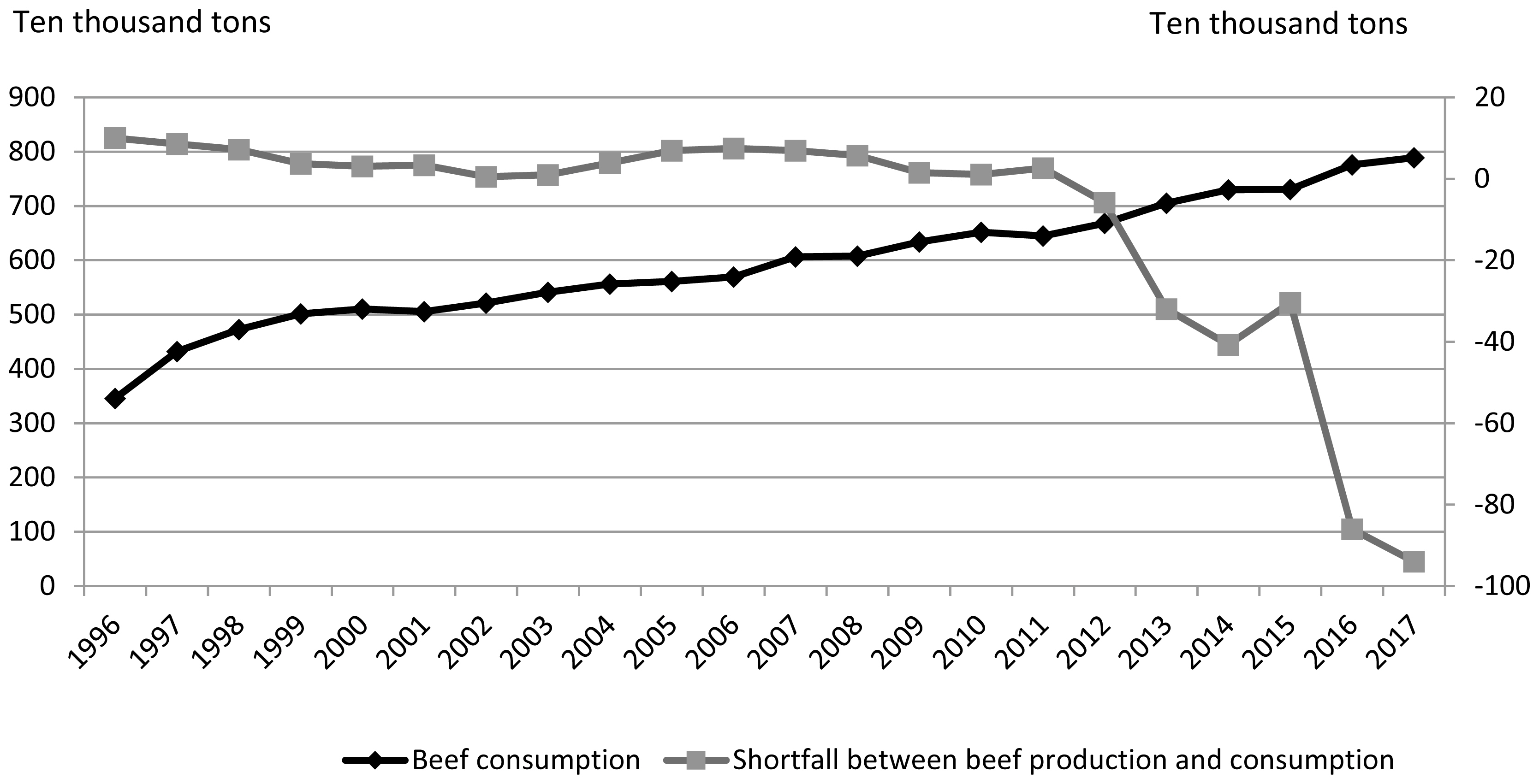

As the Chinese economy has developed over the past two decades, the standard of living of its people has greatly improved. From 1996 to 2017, there has been a rapid development in the beef market in China. As shown in Figure 3, domestic beef consumption has increased 111% from 3.5 million tons in 1996 to 7.3 million tons in 2015. Historically, beef consumption has outpaced beef domestic production. In recent years, this gap has grown from 0.6 million tons in 2012 to 3.0 million tons in 2015. Domestic beef consumption increased from 6.45 million tons in 2011 to 7.89 million tons in 2017, a 22.3% increase, while domestic beef production increased only slightly from 6.5 to 6.95 million tons during the same time, an increase of only 6.92% (Figure 3).

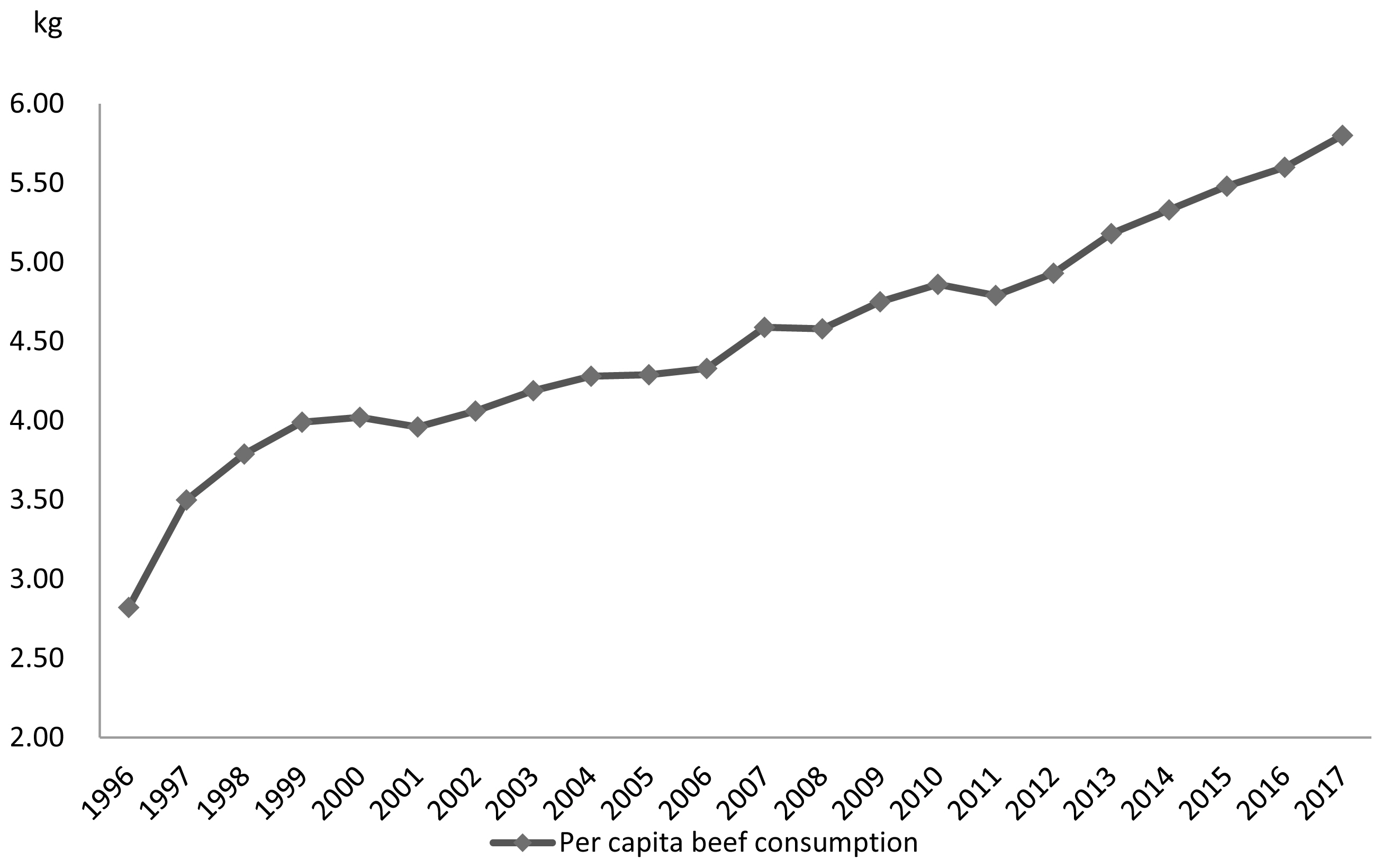

China has been one of the largest beef producing countries for at least the last 20 years [2] and also has been one of the largest beef consuming countries in the world [9]. The persistent increase in beef consumption is linked to the continuous increase in per capita beef consumption in China [10], and the market potential for beef continues to increase. Beef consumption in China was estimated at 2.8 kg per capita in 1996 and had reached 5.8 kg per capita by 2017 (Figure 4), a 107.14% increase in beef consumption per capita over the past 20 years in China. The shortfall between beef production and consumption also increased from 1996 to 2017, this is mainly due to the sharply growing in domestic demand for beef in this period.

However, China still has only low levels of per capita beef consumption compared with many more developed countries, emphasizing the potential for market growth for beef in China. Population growth in China is slow at less than 0.5% per year but is still increasing by several million additional consumers annually [4]. Continuous growth in per capita consumption multiplied by the population of China will push total beef consumption ahead of the European Union, and will be second only to the U.S. Economic growth is the principal driver of beef demand, with an emerging middle class and rapid urbanization dramatically impacting on demand for beef in China.

Chinese beef imports and exports

The role of China in global beef markets has evolved rapidly in recent years. Despite being a large beef producing and consuming nation for many years, China has not been a key player in global beef markets until recently. Since 1996, substantial changes have taken place in beef import and export trade patterns in China, and China may become the fastest-growing beef importer in the world (Figure 5). From 1996 to 2012, China was a net exporter of beef. However, because of stalled production growth and growth in beef consumption, there has been a rapid increase in beef imports to meet consumption demand in China. This has resulted in a rapid increase in official beef imports, and China has been a net importer of beef since 2013. Between 2011 and 2017, the import volume of beef into China has increased from only 20,100 tons to 620,600 tons, an increase of well over 30.88 times during that period.

China became the fourth largest beef importing country during recent years to 2015 [11]. Major beef suppliers to China between 2011 and 2015 were Australia, Uruguay, New Zealand, Brazil, Argentina, and Canada. The largest exporters of beef to China are from Australia, Uruguay and New Zealand, and the export volume was more than 85% during 2011 and 2015 [5,12].

In 2016, China emerged as the second largest beef import ing country globally. Major beef suppliers to China in 2016 were Brazil (29% of total Chinese imports); Uruguay (27%); Australia (19%); New Zealand (12%); and Argentina (9%) [13]. In 2017, Chinese beef imports was up 4.08% from 2016. Sixteen provinces (cities) including Tianjin, Shanghai, Liaoning, Shandong, Jiangsu, Beijing, Guangdong, Anhui, Hunan, Henan, Zhejiang, Fujian, Sichuan, Chongqing, Guangxi, and Hebei imported more than 1,000 tons of beef, separately. China mainly imports beef to meet its growing consumer demand, and imports live cattle mainly to improve dairy production, but also to improve beef cattle genetics. Chinese cattle have low meat yields compared to those in the main beef producing nations, hence imports of improved cattle are required to improve beef genetics and hence productivity. China’s beef import policy has been driven by domestic health and food safety issues, and the banning of imports from those countries that do not have “disease-free” cattle/beef industries. This has benefited those nations that have low disease risk and high standards of animal husbandry and food safety.

In analyzing Chinese beef exports over the past two de cades, average exports were 20,000 tons from 1996 to 2011, with peak export of 28,340 tons in 2007. Unfortunately, beef export volumes from China have sharply decreased from 22,150 tons in 2010 to 4,700 tons in 2015, or 36% annually. A reason for the dramatic changes in both imports and exports of beef in China is the rapidly increasing standard of living in China resulting in rapid growth beef consumption per capita, which has also led the Chinese population to consume more beef than before [2]. This shift has expanded the internal demand for beef in China and created a need for China to both increase the size of its beef herd and to improve the productivity of its beef cattle [4]. Destinations for beef exports from China over this period include Kirghizia, Kuwait, Hong Kong, North Korea, and Malaysia, among other countries.

On May 24, 2017, after a 14-year absence from the market, China lifted the import ban on U.S. beef. Post ban forecasts are that imports will continuously grow to reach 1.1 million tons in 2018, a 15 percent year on year increase compared to 2017. In general, the export volume of beef was always larger than the import volume before 2010 because the market price of beef in China had long been below that of the developed countries. However, the price of domestic beef rose rapidly since 2010 due to the increasing demand in China.

Beef prices in China

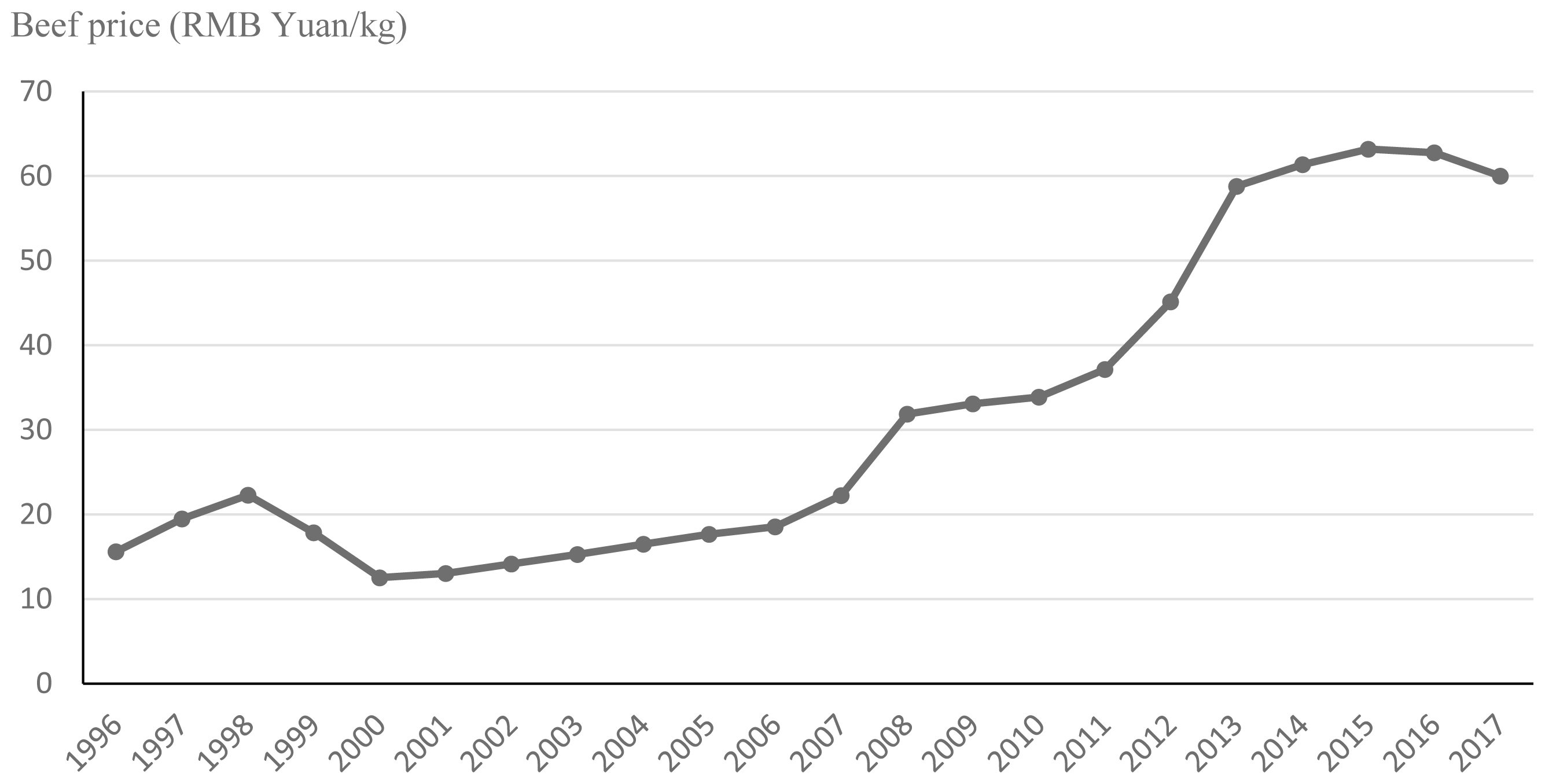

China faces a situation in which both demand and the average price for beef are increasing. The economic definition of rising prices and rising consumption is demand growth. Underlying demand and supply forces have exerted strong upward pressure on beef prices in recent years in China. The beef price increased by 379% from 12.53 Yuan/kg (CNY) in 2000, which was the lowest beef price during the past two decades, to 60.0 Yuan/kg (CNY) in 2017 (Figure 6). In China, prices of beef are greatly influenced by market demand and feed costs. The rapid increase in the price of beef in China was likely a result of reduced beef production and the increase in domestic market demand. In the most recent two decades, extraction rates show that the percentage of cattle slaughtered relative to the total cattle inventory increased sharply, heavily exceeding 25% (Figure 1) which is the commonly held safety criteria for slaughter percentage of cattle to maintain cattle inventory. The high price of beef has made beef finishing more profitable, resulting in a sharp rise in this extraction rate between 1996 and 2015 in China [4]. In addition, corn is a major component in the finishing diet of beef cattle and the price of corn has had a major impact on the cost of fattening beef. The price of corn in China increased sharply between 2009 and 2014 [14], during which time the price of beef doubled (Figure 6). As the price of beef continues to rise in China, fattening of “bull calf-fed” Holstein become the part of the stable source of beef cattle industry in China.

FUTURE PROSPECTS FOR BEEF PRODUCTION IN CHINA

From the data presented herein, China is now a major player in the both the world and regional beef industries in terms of production, consumption and trade of beef. However, although average beef consumption per capita in China has increased, it remains much lower than other developed countries. For the past several years, the increase in beef sales and a shortage of cattle for finishing feedlots has led to a decrease in cattle inventory and finished beef available for slaughter. The beef production industry in China is still operating at low efficiency due to various factors including the lack of high-performance breeds optimized for local conditions.

Post forecasts 2018 production will reach 7.1 million tons, about a 0.5% increase from 2017. Most of the production gains will come from larger scale farms. Despite beef prices being down slightly in 2017, the price is still strong and has been stable since the end of 2013. China National Reform and Development Commission [12] has a plan to expand beef production to 8.0 million tons by 2020, which represents an average annual increase of 2.0%. The China National Development and Reform Commission plans to increase extraction rate to 55%, with farms with at least 50 cattle slaughtered per year responsible for a major portion (40%) of Chinese beef production.

With the rising income level and the changes of dietary habits of Chinese residents, the demand for beef per capita will significantly rise in the coming ten years, bringing about the rapid growth. The amount of beef in Chinese diets has increased. Taking into account China’s large population, the wide disparity of beef consumption in China compared other developed countries, increasing gross domestic production and consumption of beef in China, and limited growth in Chinese beef production, we estimate that the ratio of beef imports to exports will continue to increase in China. Beef consumption is estimated as 5.5 kg per capita with an annual increase of 1.13% across China’s population of 1.45 billion. A small rise in per capita beef consumption from the current low levels in China would create further significant demand for beef. At the current population, every 100 gram increase in per capita consumption will require about 140,000 tons of beef. Economic growth is the principal driver of beef demand, with an emerging middle class and rapid urbanization dramatically impacting beef demand. As discussed previously, population growth in China is slow, at less than 0.5% per year, but still adds several million additional consumers each year. China’s per capita beef consumption was about 5.8 kg in 2017 and industry estimates it will reach 6.0 kg in 2018. Although this increase is significant, China’s average per capita beef consumption remains well below 8.6 kg/person—the current world per capita average. However, China is projected to continue increasing consumption, which bodes well for future growth in this market. Furthermore, as a result of stalled production growth, the demand for beef in the Chinese market is estimated to rise during 2018 to 2020 with the growth of economy and will continue to result in more rapid increases in official beef imports. The import volume of beef in China is expected to increase due to the limited growth space of the domestic beef production. There will be quite a lot of opportunities in the Chinese market for breeding, processing and trading enterprises worldwide. By 2020, China’s net beef imports will be about 0.5 million tons.

The long-term, sustainable development of the Chinese beef industry is an important issue for China. It has been emphasized in this review that beef consumption in China will continue to grow rapidly. The heavy imbalance between beef supply and demand in China predicts continued growth of beef imports. Although some breed improvement work has been done in the past years, most of the Chinese beef cattle inventory remains low-performance. Based on this, cattle breeding system should be strengthened, and selection should be made to improve the carcass yield of individual cattle. And some critical measures should be taken to improve the performance of native cattle breeds and creating new cattle breeds with better adaptability for local resources and environment.

Associated issues that need to be addressed include pres ervation of and breed selection for the national cattle herd, sustainable development of cattle co-operative organizations, better marketing systems, increased subsidies for improved cattle genotypes, and adaption of production systems to better meet consumer demands. Some key technologies, such as embryo transfer, artificial insemination, scientific feeding management of beef cattle should be continuously extended to cover more individual cattle in beef cattle raising regions. The application of these technologies can increase the reproduction ratio, the number of cows and the survival rate of calves and can shorten the length of the beef production cycle to further save costs and decrease the cost per unit of output.

Calf-crop operation is the key scenario for Chinese sus tainable cattle industry, because the shortage of calves available to finishing feedlots is the biggest limitation to the development of the beef battle industry. The government should take more action and conduct more researches into improving the production efficiency of beef cows and calves and implement incentives to make calf production more efficient and more profitable. Currently, Chinese beef consumers are looking for high-quality and named brands. Proliferating ecommerce platforms offer increasingly convenient ways for retailers to market high-end beef through the internet. For example, most steaks for in-home consumption are sourced from e-commerce platforms. Thus, a system of guide beef consumption is necessary for Chinese consumer. High quality beef should have excellent price by the scientific judging of the national beef grading system. Moreover, a better organization of the beef production and supply chain as part of a sustainable system will also need to consider other issues such as environmental protection, animal welfare, national policy support, land use, bank loans, insurance services and financing services.

In conclusion, to enhance national beef cattle industry growth, improvements in organization, cattle management and genetics, and technology are required. These issues might serve as a future reference for ensuring the adequacy and efficiency of the beef supply and the sound development of the domestic beef industry in China. The long-term, sustainable development of the Chinese beef industry is an important issue for China.

PDF Links

PDF Links PubReader

PubReader ePub Link

ePub Link Full text via DOI

Full text via DOI Full text via PMC

Full text via PMC Download Citation

Download Citation Print

Print