Current situation and future prospects for beef production in Europe — A review

Article information

Abstract

The European Union (EU) is the world’s third largest producer of beef. This contributes to the economy, rural development, social life, culture and gastronomy of Europe. The diversity of breeds, animal types (cows, bulls, steers, heifers) and farming systems (intensive, extensive on permanent or temporary pastures, mixed, breeders, feeders, etc) is a strength, and a weakness as the industry is often fragmented and poorly connected. There are also societal concerns regarding animal welfare and environmental issues, despite some positive environmental impacts of farming systems. The EU is amongst the most efficient for beef production as demonstrated by a relative low production of greenhouse gases. Due to regional differences in terms of climate, pasture availability, livestock practices and farms characteristics, productivity and incomes of beef producers vary widely across regions, being among the lowest of the agricultural systems. The beef industry is facing unprecedented challenges related to animal welfare, environmental impact, origin, authenticity, nutritional benefits and eating quality of beef. These may affect the whole industry, especially its farmers. It is therefore essential to bring the beef industry together to spread best practice and better exploit research to maintain and develop an economically viable and sustainable beef industry. Meeting consumers’ expectations may be achieved by a better prediction of beef palatability using a modelling approach, such as in Australia. There is a need for accurate information and dissemination on the benefits and issues of beef for human health and for environmental impact. A better objective description of goods and services derived from livestock farming is also required. Putting into practice “agroecology” and organic farming principles are other potential avenues for the future. Different future scenarios can be written depending on the major driving forces, notably meat consumption, climate change, environmental policies and future organization of the supply chain.

INTRODUCTION

Human beings have been consuming beef since the beginning of humankind and, following domestication of bovines, beef production has developed in all countries of the World. Today, beef production in the European Union is ranked third in the world with almost 8.0 million tons of carcasses in 2018 [1]. Not only does beef production contribute considerably to European food security and sustainable land use, but also to the socioeconomic well-being of rural communities, and to the gastronomic pleasure of urban and rural consumers across the continent. Nevertheless, the beef industry in Europe is now facing a number of serious challenges based on expectations of European consumers [2].

Environment and welfare

First, public concern indicates a demand for more control of animal welfare and environmental impact, in particular for intensive young beef cattle fattening farms. Indeed, there is evidence that some beef production systems have a negative environmental impact. Beef cattle farms can contribute significantly to the production of natural greenhouse gases. High emissions of methane from enteric natural fermentation and nitrous oxide from excreted nitrogen mean that beef farming has gained a reputation as one of the most polluting food production systems. However, amongst beef production systems, some of those in Europe are the most efficient and least polluting in the world [3]. Furthermore, goods and services provided by livestock farming are numerous and sometimes forgotten or undervalued [4].

Quality

Second, there is more and more emphasis on delivering the beef quality expected by the consumer. It has been suggested that red meats contribute to human health problems [5] and this has received a lot of publicity. However, beef also delivers many important nutrients [6]. Occasional authenticity and safety issues also present a challenge to the beef industry [7,8]. In addition, the consistency of eating quality does not always meet consumer expectations for a high price product [9].

Consumption

Third, EU consumption of beef reached a high in 1985 at 25 kg per person per year, but from then has steadily declined to 16 kg carcass equivalent. This is now low compared to other countries in the world, e.g. 37 kg in the USA, 36 kg in Brazil and 59 kg in Argentina [1].

Diversity

Unlike its main competitors, Europe has a wide variety of beef farming systems and supply chains, with production systems developed to suit the varied geographical, climatic, economic and societal needs of different regions of the continent [10]. While some systems are very efficient in terms of environmental impacts or on an economic basis, others are much less so, but may play an important role in land management and rural vitality. This diversity makes the industry very complex and presents a challenge to the implementation of new innovations.

Disconnected supply chain

Across Europe, there are many different types of supply chains and some work more effectively than others. Often, there can be a lack of trust and understanding between the different parts of the supply chain, and the mechanisms for delivering value to the primary producer are not always clear or understood. All of these challenges have an adverse impact on the entire supply chain but especially the farmer, and beef production at the farm level is often of marginal profitability [11].

Beef and society

Farm animals do not only act as economic resources but also contribute to the culture of both rural and urban dwellers. In many regions of the world, beef animals contribute to land management and help to sustain the rural social infrastructure by providing employment and are part of the rural “way of life”. However, the current exposure of meat production systems to the public has raised new social questions about environmental issues, human health, and animal welfare and, indeed, whether animals should be slaughtered for human food [reviewed by 12,13].

Despite these challenges, the beef industry in Europe has many strengths. Its diversity results in a wealth of production practices, some of which are already addressing the challenges described. A large amount of scientific research has been published on all aspects of beef production including its economic performance [reviewed by 10], its impact and sustainability [reviewed by 3], its nutritional value [reviewed by 14] and its eating quality [reviewed by 15]. However, uptake by the industry has been irregular. Indeed, transfer of knowledge and innovation from science to the industry is weak in the meat sector and needs to be strengthened [16]. An increasing engagement between those engaged in the beef supply chain and beef scientists aims to address this issue. Future projects and research should help beef producers and the European beef industry work together with scientists in all disciplines (biology, farming systems, process, social and human sciences, economics) to address these challenges.

This article will review, in its first part, the relationships between human beings and farm animals from bovine domestication until current times in developed countries such as in Europe. The current economic situation of beef production and consumption in Europe will be detailed in the second part. In the last and third part of this article, the evolution of consumer expectations will be described in order to conclude with the challenges and future prospects of the European beef industry

HUMANS AND MEAT

Evolution of meat consumption

Human beings have eaten meat since the origins of the humanity [17]. Indeed, the first proteins coming from animals could have been those from insects and from scavenging the carcases of herbivores.

Gradually, the human-animal connections became increasingly complex, as the first scavengers became hunters [17]. This led to a domination of animals by humans, with humans becoming hunter and animals becoming game. This power balance is widespread across nature, with many animal species being predators and consuming others. The development of cooking methods (linked to the controlled use of fire) and well organized and efficient hunting allowed meat to gain in importance in the human diet. Hunting, cooking and preservation methods became more complex and elaborate with the development of human societies.

Along with the Neolithic Revolution, came the settlement of human populations and also the development of vegetable cultivation and the domestication of animals [17]. This major step modified relationships between humans and animals, by strengthening the influence of the first one on the second. The first animal to be domesticated in Europe and Asia was the dog. Tamed from the wolf, the dog was first used for hunting. Then came other animals (pigs, bovines, and small ruminants such as goats and sheep) that were domesticated for their products, especially meat and milk, which remain staple foods for many human societies. Thus, throughout history, humans and animals have been closely interlinked, evolving jointly. During most of this period, civilizations were mostly rural, and production and consumption were occurred close to one another. The urbanisation of human societies, and the consequent separation of production and consumption has brought new challenges, of ensuring safety and quality of the end product to the consumer [18].

Over time, meat production has been refined, with improve ments based on experience, technological developments and, latterly, scientific research. Breeding practices, slaughtering, cutting and ageing processes have become increasingly advanced, with a wide range of methods to preserve meat for extended periods. Across different countries, numerous regional meat products have been created based on fermentation, salting and, more recently, cold chain and freezing technologies.

Meat marketing began to develop during antiquity. First, different price-lists appeared for various pieces of meat. After centuries of evolution, meat began to be a commercial product, traded around the world. This came along with industrialization and the growth of urban populations, the expansion of meat processing capability and distribution networks. This led to the need for trading rules to describe the product being bought and sold [18]. The constant evolution of markets (but also of their rules) required continuing adaptation of the meat producers and traders. This led to recurring difficulties, such as the balance between high and low quality meat and the disconnection between supply and demand. To meet market and consumer needs, high quality sectors were developed, leading to the creation of i) official labels linked to product origin, or guaranteeing its sensory or nutritional quality, ii) certified products, and/or iii) commercial marks.

Evolution of relationships between humans and meat

The above evolutions do not take account of the social aspects of meat consumption, such as the gustative and friendly pleasure associated with meat consumption in families or social gatherings. There are also considerations that are specific to meat products, such as symbolic, religious, ethical or moral interests. In many cultures, it is considered necessary to kill animals to eat in order to sustain life, and a natural evolution of the relationship between predator and herbivores. The first meaning of “meat” (vivenda) was “what is of use for life”. However, in some other cultures, meat consumption is forbidden [reviewed by 12]. In past times, the consumption of meat was often the preserve of the wealthy with poorer people eating very little meat, while, in other societies, meat consumption was associated with religious sacrifices, now that consumers in the western world have a considerable choice of foods, there is an ongoing debate on the morality of killing animals for food. In modern times, the evolution of vocabulary (“slaughter” instead of “killing”), the location of slaughterhouses away from human habitation and the creation of processed products have distanced the consumer from the origin of meat. Nowadays, the urban consumer is sufficiently remote from farms and animals to forget that meat comes from an animal that has been alive.

Food consumption requires a big trust in the product that we ingest, and in the suppliers of this product (the breeder, producer, processor and retailer). This explains why sanitary crises have always had a strong impact on consumer habits. For instance, after the bovine spongiform encephalopathy crisis, the meat sector found it necessary to completely reorganize its procedures. This has led to a significant increase in animal controls and inspections, and the introduction of a system of total meat and carcase traceability, aiming to prevent sanitary crises where possible, and to ensure a maximal response in case of problems arising.

If consuming a farm animal is acceptable to many people, the idea of eating a pet is generally not conceivable. This question raises two important issues: first of all, certain animals have lost their edible status by acquiring a pet status, reducing de facto their attraction as edible animal (historically, this has been the case for dogs; it is nowadays the case for horses or rabbits). This may be partly related to the absence of widespread hunger in the western world, possibly for the first time in history.

The world human population is anticipated to reach 9 bil lion by 2050, and this is a 30% rise from the population in 2010. The challenge of how such a population may be fed from the finite world resources is challenging food producers and governments. It will not be feasible for the beef industry to grow to meet demand, as grasslands are finite and it is proposed that it will be necessary to moderate consumption of meat, especially ruminant meats [19]. For this reason, other sources of proteins are being developed nowadays, for example proteins stemming from insects [20]. This reminds us of the diet of hunter/gatherers at the beginnings of humanity.

The philosophic point of view

Many philosophers, such and Leroy and Praet [21] have theorized the evolution of relationships between humans and animal/meat, by distinguishing 4 phases:

The first one is called “deference” and corresponds to the prehistoric period. Man was both hunter and gatherer. During this period, man respects animals as living subjects, not really related to him.

The second phase corresponds to animals’ “domestication”. Animals become “subjected” living beings. During this period, availability of meat-based products remains modest.

The third phase is “denial”. The previous trends are ex-aggerated, as meat becomes an accessible and plentiful product. This period is characterized by a denial that animals are sensitive beings. Indeed, they are, most of time, considered as objects, as previously described in the animal-machine concept of Descartes [22]. The slaughterhouses expand far away from consumers. The link between animals and meat become blurred.

The last phase is referred to as “disgust”, as Man becomes aware of previous exaggerations and becomes conscious of the need to respect animals, which are once more considered as sensitive beings. For many people, this corresponds to the present time.

Other philosophers, such as Wolff [23], suggest that the status of animals is directly related to the relations that human beings cultivate with animals. Thus, the status of the animal depends on the situation. Man’s duties and attitudes to animals differ, depending if animals are pets, productive animals or wild animals. Man engages in a diversity of relations with the various members of the animal kingdom (from flea to dog). Thus, man’s duties toward animals depend on the nature of these relations. This philosophic approach argues that the movement, which assigns a value to the animal, considered as a unique being (known as “modern animalism”), contains several contradictions. First of all, man is sometimes included, and other times excluded from animal kingdom. Secondly, it is easily conceivable that dogs and their fleas cannot be handle in the same way. Wolf proposed that the main cause of the complex and contradictory relationships between humans and animals is that Man has lost awareness of the uniqueness of humankind according to Wolff [24].

ECONOMIC SITUATION OF BEEF PRODUCTION AND CONSUMPTION IN EUROPE

Key figures for the European Union

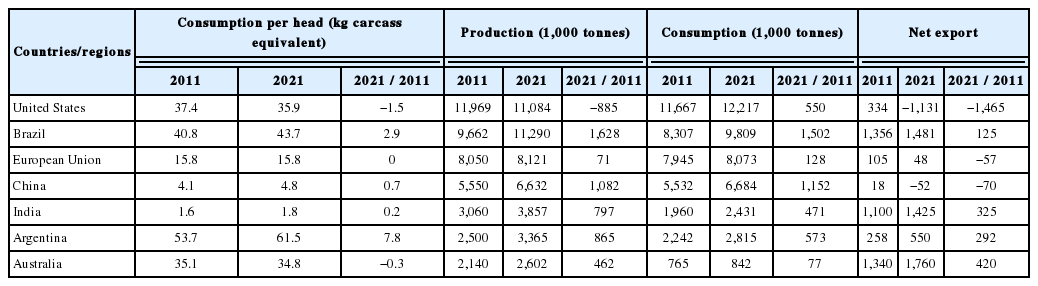

The United States, Brazil and the European Union produce roughly 47% of the world’s beef, with these countries producing about 19%, 15%, and 13%, respectively (http://beef2live.com/story-world-beef-production-ranking-countries-85-106885, Table 1).

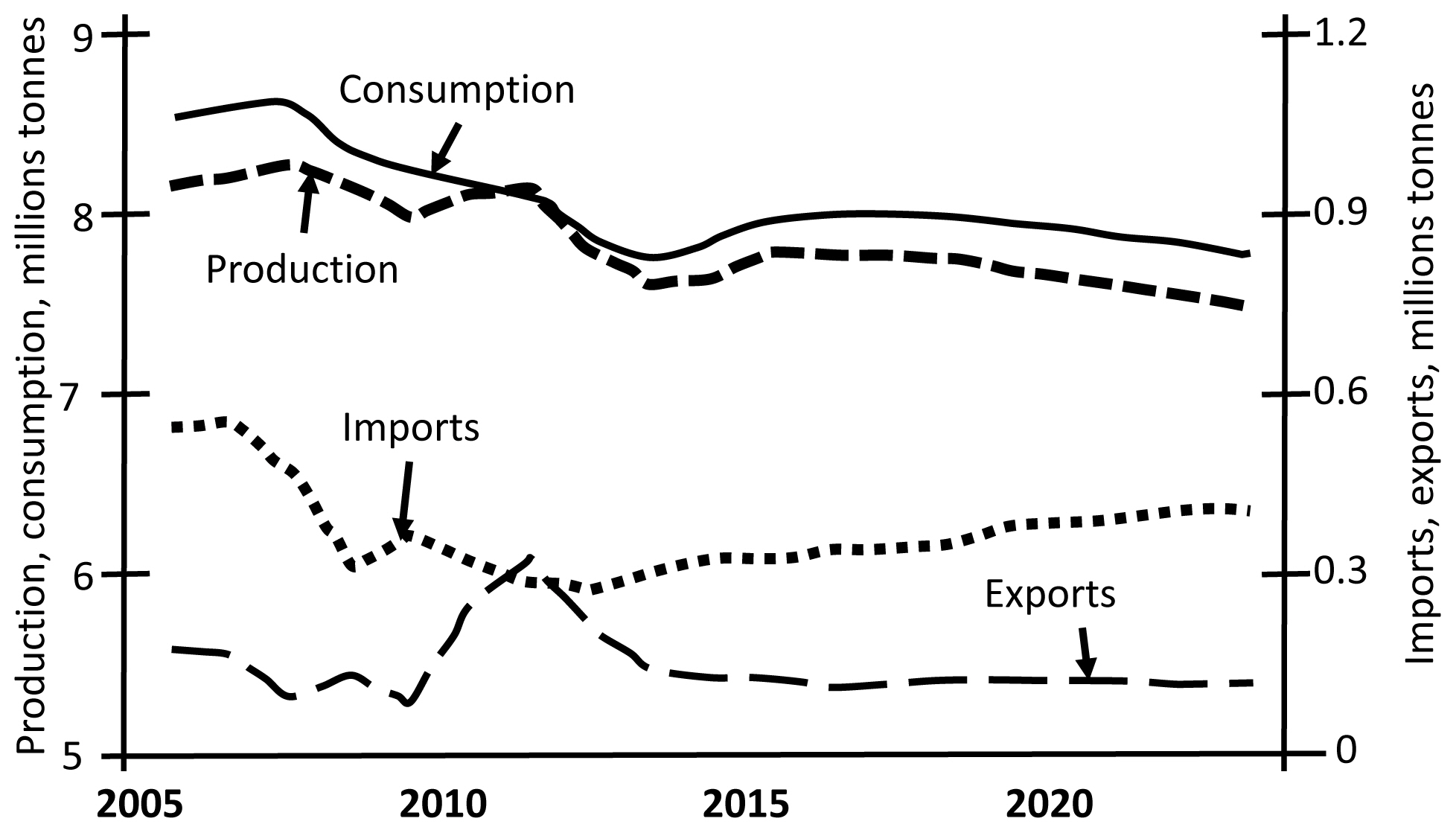

Beef consumption, production and export in major beef producing countries/regions in 2011 and in 2021 (projections)

The total meat consumption in the European Union per capita has barely changed since 2000. On average, European consumers eat 78 kg of meat per year [1]. However, the proportion of the different meat types consumed has significantly changed since 2000; while European consumers eat 20% more of poultry meat, and 33% less of sheep and goat meat, the consumption of beef has declined by only about 10% during the same period.

On average, beef consumption is Europe is about 16 kg per capita (20% of total meat consumed). This proportion of beef consumption is less than that observed in Argentina, Brazil, the United States, and Australia (Table 1), where beef represents 55%, 41%, 34%, and 37%, respectively, of the total meat consumption [1]. Total beef consumption is likely to increase from 2011 to 2025 with the lowest increases in Australia and in the European Union and the highest increases in Brazil and China. Similarly, the highest increases in production are likely to occur in Brazil and China from 2011 to 2025 and the lowest in the European Union, and especially in the United States, which are likely to produce less beef in 2025 compared to 2011. Exports of beef are likely to increase from 2011 to 2021 from the major countries except for the European Union and China and especially for the United States (Table 1).

Key statistics for European countries

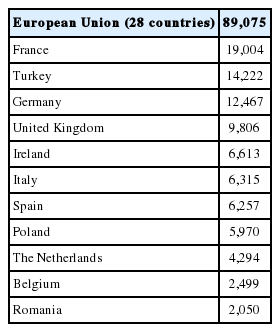

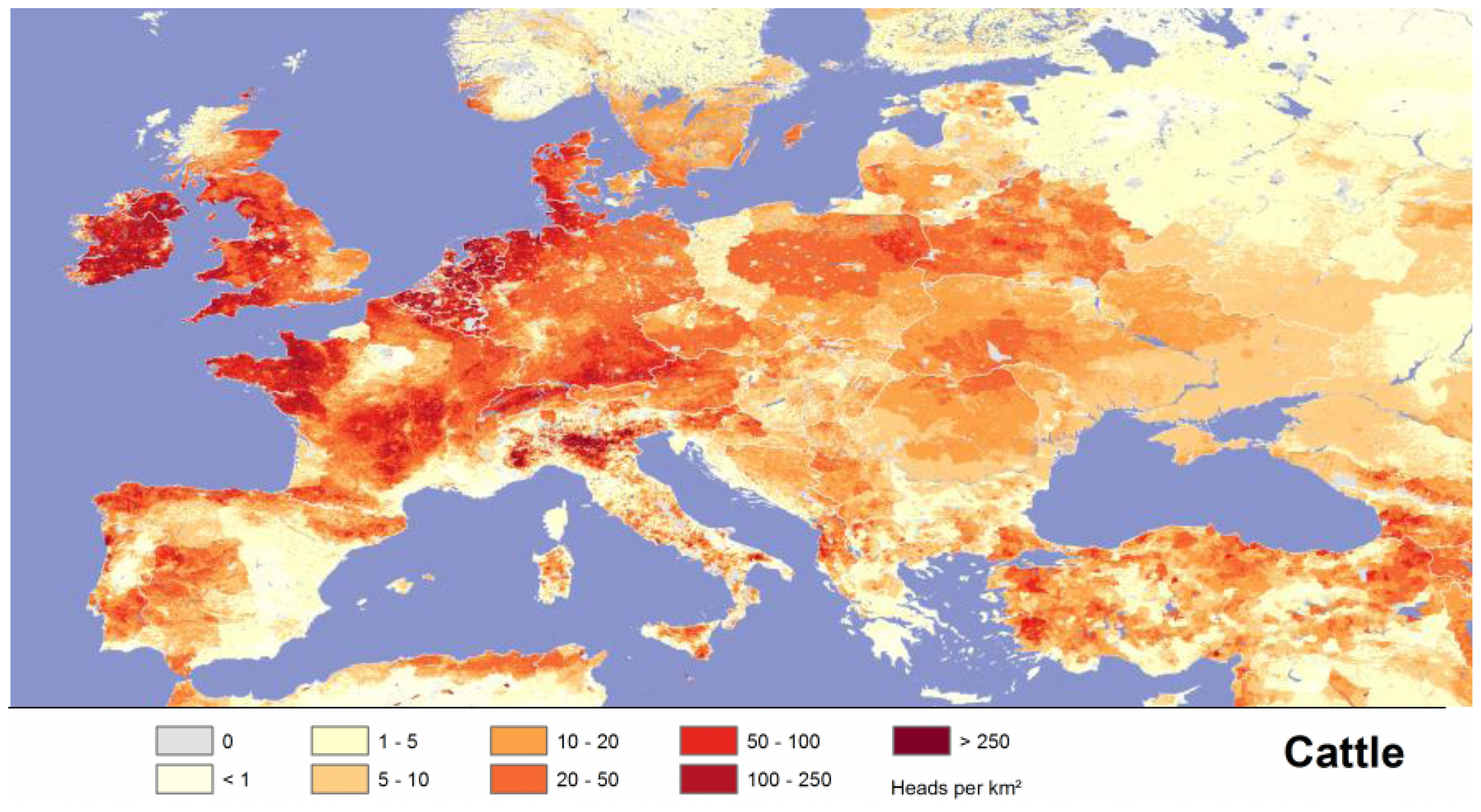

More than 89 millions of cattle of meat or dairy type are present in the European Union, with the largest herds in France and Germany. Turkey, which is outside the European Union is also characterised by a high number of cattle (Table 2). Cattle are heterogeneously distributed across European countries (Figure 1). Furthermore, most of the meat bovine herd is located in France (34.4%) but also Spain (15.2%), the United Kingdom (12.8%), and Ireland (8.7%) (http://ec.europa.eu/eurostat/statistics-explained/index.php/Meat_production_statistics#Beef_and_veal_28bovine_meat.29). More precisely, at the regional level, the numbers of non-dairy cattle are the highest in Ireland, Bayern (Germany), The Netherlands, Pays de Loire (France), and in Mazowsze and Podlasie (Poland), all these 5 regions having 22% of the total number of non-dairy cattle (2016 report). The stocking density of fattening farms (in livestock unit par ha of utilized agricultural area) is the highest in regions of Northern Italy and of the Benelux [10].

Total cattle numbers (thousand heads) in the European Union and in major European countries in 2014

Population density of cattle (head per km2) in the European countries. http://livestock.geo-wiki.org/graphics/

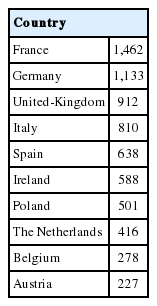

Almost 8 million tonnes of bovine meat are produced in the European Union. The highest production of beef meat is in France and then in Germany (Table 3). The average carcass weight increased by about 24 kg/head from 2000 to 2015. From 2006 to 2015, the major changes in total volume of cattle slaughtering in Europe were observed in Poland (+32.6%) and in Romania and Bulgaria (−77%), Slovakia (−61%), Estonia, Greece and Italy (around minus 30% to 34%) [10].

Beef production (thousand tonnes) in Europe in 2016

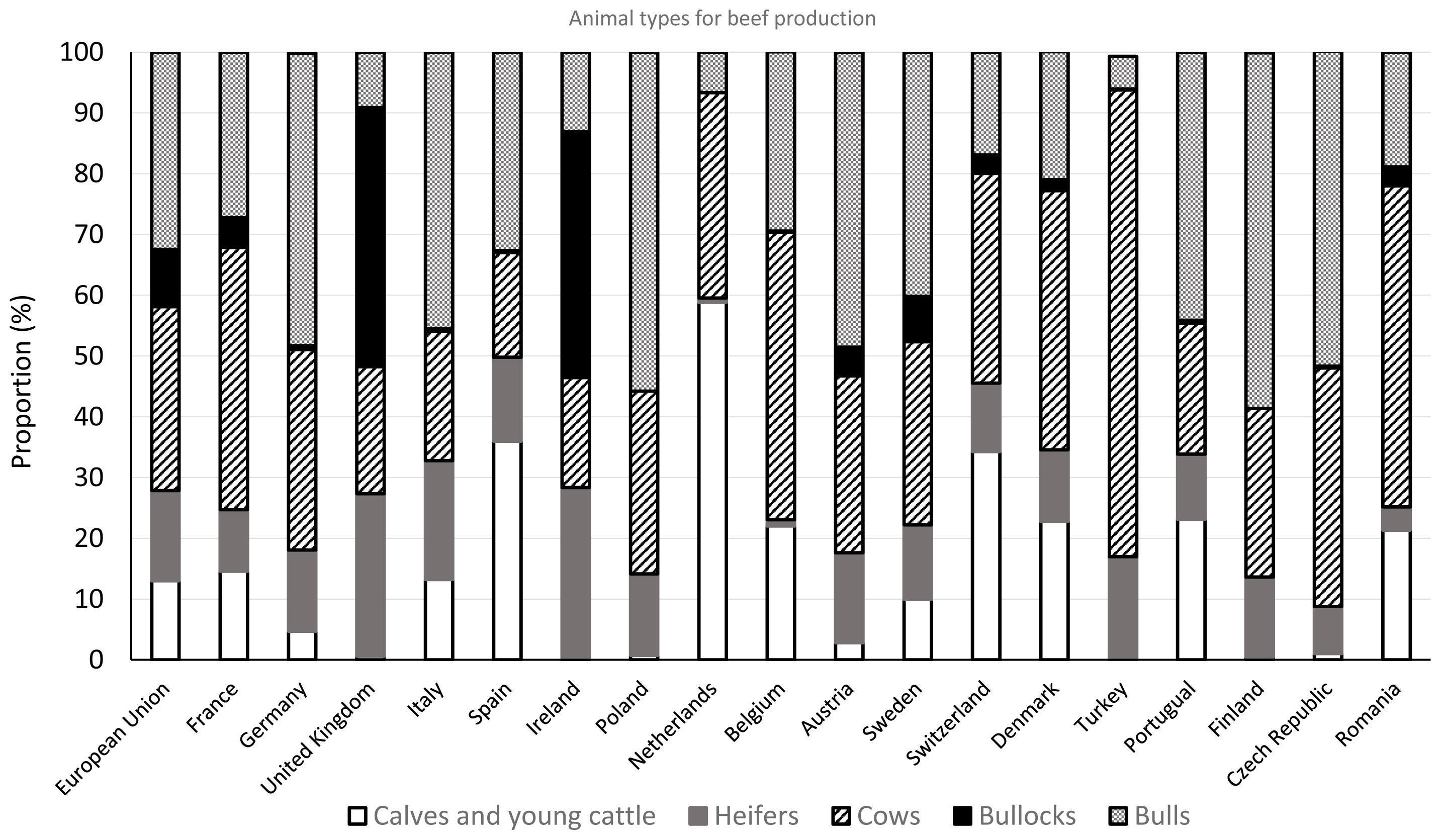

Beef production varies widely across European countries in terms of animal types (Figure 2):

Production of beef and veal, by class of bovine animals, 2015. Adapted from http://ec.europa.eu/eurostat/statistics-explained/index.php/Agricultural_production_-_animals

a high production of meat from young animals (calves and young cattle aged not over 1 year) is observed in The Netherlands (58.8%), Spain (36.0%), and Switzerland (34.2%);

a high production of beef from steers/bullocks (which are castrated bovine animals aged 1 year or more) is observed in the UK and Ireland (42.6% and 40.5% respectively);

a high production of beef from bulls (non-castrated male bovine animals aged 1 year or more) occurs in Finland (58.5%), Poland (55.8%), Czech Republic (51.8%), Austria (48.5%), Germany (48.1%), and Italy (45.6%); and finally;

Turkey and Romania produce beef mainly from cows (76.8% and 52.8%, respectively).

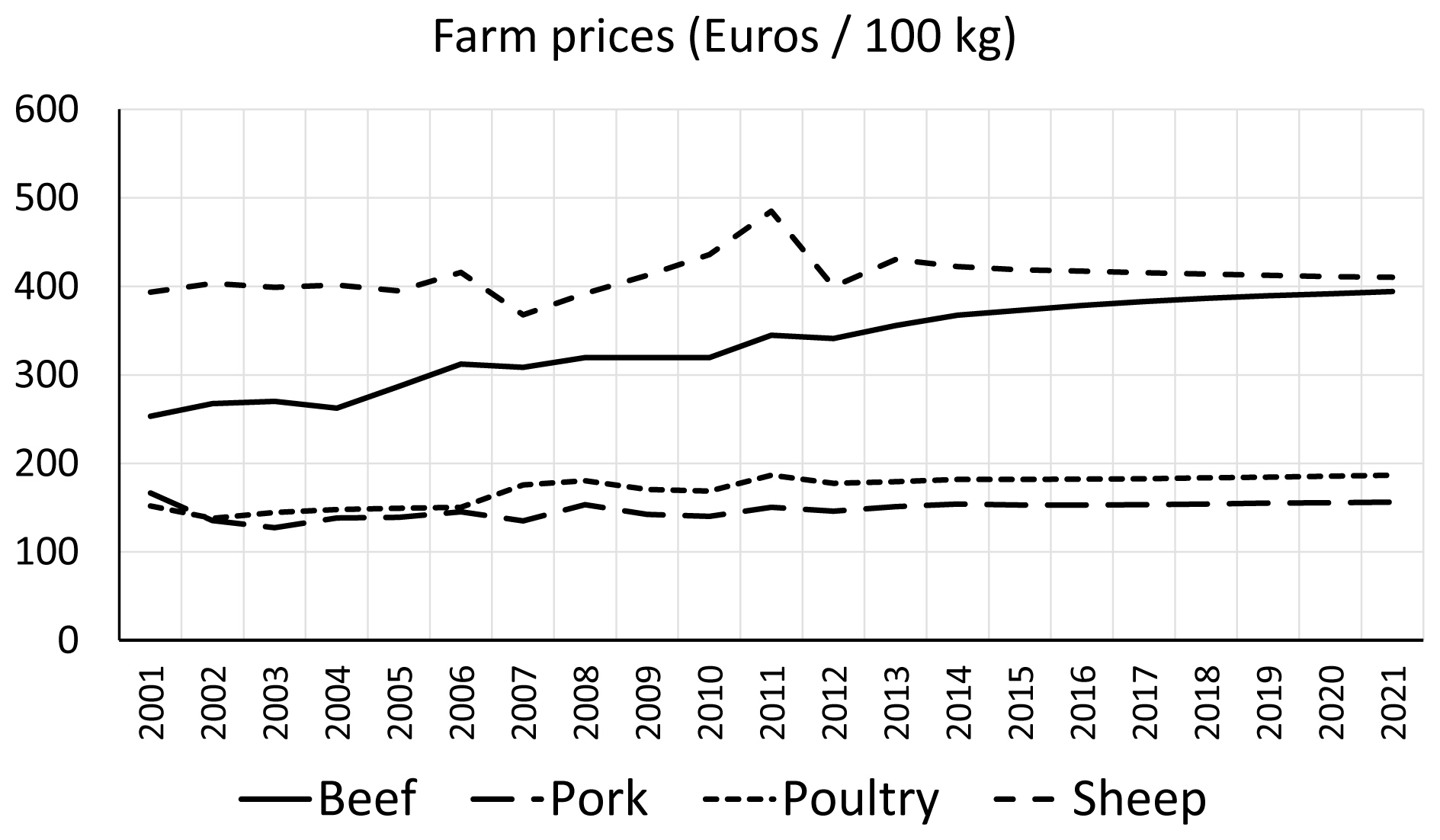

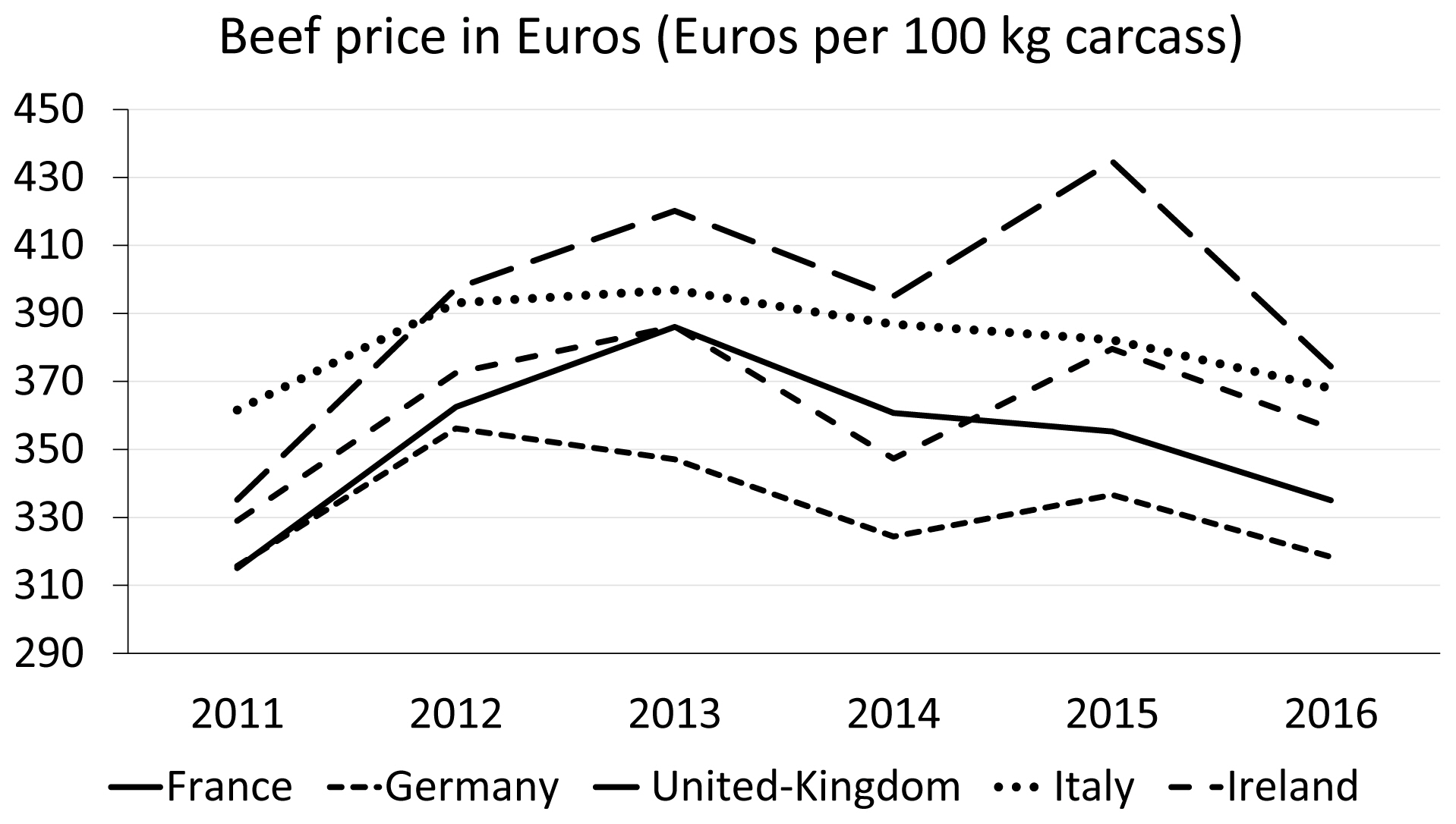

Cattle slaughter prices of different cattle types (steers, young bulls, cows, heifers) increased, in current currency not taking inflation into account, on average from 2.5 euros in 1991 to almost 3.8 euros per kg in 2015 [10], especially from 2010 to 2015. It is forecasted that it will continue to increase to reach 4.0 euros per kg, so that beef meat and sheep meat will have the same farm prices, and so that beef meat is likely to become even more expensive than pig and poultry meats (Figure 3). However, cattle slaughter prices slightly differ across the European countries with the largest cattle herds (Figure 4).

Beef price in Euros (per 100 kg carcass in France, Germany, United Kingdom, Italy, and Ireland from 2011 to 2016. Adapted from: www.agreste.agriculture.gouv.fr/conjoncture/le-bulletin/

Specialist cattle fattening farms and beef producers in European countries

The highest number of specialist cattle fattening farms is located in Ireland, followed by North-Western Spain (especially Galicia and Asturias), in or around the Alps, in Eastern Poland and in Slovenia. This regional concentration can be evidenced by the fact that 32% of cattle fattening farms are present in Ireland, Galicia, Asturias, Slovenia, Mazowsze, and Podlasie. By contrast, the lowest regional farm numbers are found in East Germany and in several Mediterranean regions. In comparison to all other regions, regions with the highest numbers of fattening farms tend to have the lowest average farm sizes: the largest farms are observed in the Benelux and Germany, whereas the smallest farms are observed in the North-Eastern regions of the European Union. However, farm sizes tended to be more homogenously distributed than farm numbers [10].

The productivity per animal of specialized cattle fattening farms (measured as the total annual livestock financial return per livestock unit) differs a lot across European countries. In fact, it differs by a factor of eleven, which means than animal productivity is eleven times higher in Denmark (3,787 Euros per animal unit) than in Latvia (344 euros per animal unit), one of the three Baltic states. The highest productivity is found in and around the Benelux, in and around the Alps, in North and Central Italy as well as in Finland [10]. However, input costs also vary between countries. To take account of this, the input cost productivity of bovine meat production (the ratio between the annual value of meat and the total input costs) shows a decreasing trend across European countries from the South-West to the Northeast. It is the highest in the Iberian Peninsula and in some parts of Italy (between 97% and 162%) and the lowest in Slovakia (10%), Denmark and some Swedish regions (17%) [10]. Thus, beef production in Europe is, at best, of marginal profitability.

Farm incomes of fattening farms are heterogeneously dis tributed across European countries and within each country. The highest income per farm is in Veneto in the Northeast of Italy (107,213 euros per year) and the lowest in Slovenia (2,365 euros). More generally, the highest regional farm incomes are in Northern Italy, the Czech Republic, the UK and Northern Finland and the lowest in Poland, Southern Sweden, South-West Germany and Slovenia [10].

Labour income is rather lower compared to other agricul tural systems (Figure 5) and also very heterogeneous but with a different pattern. It is the highest in Northern Italy, Northern Spain and Northern Finland with the highest value in Veneto (72,415 euros). It is the lowest in some parts of Germany, France and Spain but especially in Eastern countries: Slovenia (1,985 euros) and Slovakia (2,178 euros), which means a difference of 35 fold. The ratio of labour income in fattening farms to the regional average income is very high in Veneto (242%) with the other high values being observed in the Iberian Peninsula and Latvia (96% to 110%) and the lowest (8%) in Hessen (Germany) and Slattbygdslan (Sweden), and to a lesser extent in Slovenia (11%) and Luxembourg (15%) [10].

Income level of all agricultural systems (Total) compared to “specialized cattle farms” in the EU. Source FADN http://ec.europa.eu/agriculture/rica/database/database_en.cfm

The contribution of specialised cattle farming in the agri cultural sector (as measured by its share of total farm numbers) varies from 1% (Southern Spain) to 73% (Northern Spain). This contribution is the highest in Northern Spain (Asturias, Cantabria), central France (Limousin), and Ireland, Sweden and Scotland and the lowest in regions bordering the Mediterranean Sea.

The share of the total regional labour force varies from 0.02% to 0.04% in England-East and Central Germany to 2.4% to 2.7% in Ireland, Limousin (France), and Asturias (Spain) [10].

Price, production costs, and supply chain

Over the past twenty years, the Common Agricultural Policy has provided subsidies to compensate for low farm meat prices. Specific support was given to grassland or extensive farming systems. Despite this, in some regions such as in the Centre of France, the farm income remained on average among the lowest of the French farms. The constant increase in farm size and labour productivity (by 30% to 80% in 20 years in the centre of France) and the simplification of livestock rearing practices in the centre of France did not allow any increase in net income per worker in constant currency despite European subsidies [25]. In fact, different strategies were used in different European countries; in France and also the UK, farmers invested in more equipment and mechanization whereas, in Spain and Ireland, farmers invested less and modified their production systems less, making them being more economically efficient. However, in all cases, and despite European subsidies, incomes in specialised beef farms remain lower than those of other agricultural production systems [11] (Figure 5).

On average, in the European Union, the farm price is 379 euros per 100 kilograms and is likely to increase to 394 per 100 kilograms in 2021 [1]. Since 2005, production costs of beef finishing farms around the world have been increasing. Between 2005 and 2015, they were up by 14% for the European systems, by 114% for the Brazilian systems and by 35% for the American feedlot system (Figure 6).

Evolution of the production costs of beef finishing farms. Source: GEB_ Institut de l’élevage from agri benchmark (www.agribenchmark.org).

Many reasons explain this increase:

The volatility of feed and energy prices, which began in 2008 until the middle of 2012 and 2013, resulted in increased production costs. The prices never came back to their pre 2008 level.

The recurring droughts in the USA, Canada, Australia and Brazil, as well as the shortage of store cattle in Argentina have also contributed to increased production costs.

Land prices in Brazil have doubled over the last decade because of the strong competition between beef, cotton and cash crops,

Finally, the evolution of exchange rates were connected to policies or economic crisis of some countries such as Europe, Brazil.

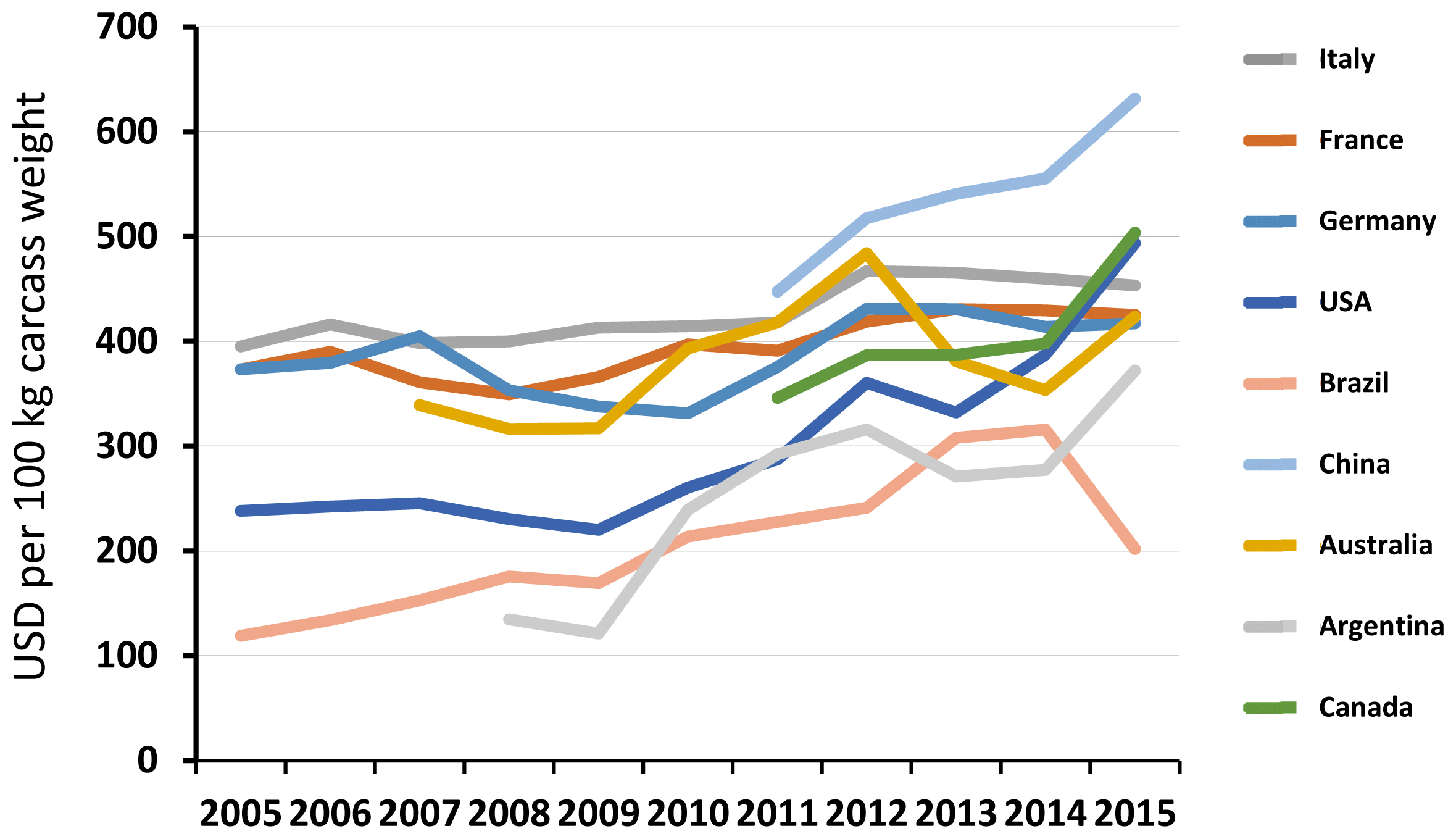

The differences between grain-finishing systems (Argentina, US, Canada), pasture systems (Australia, Brazil) and European systems remained the same even if year after year the gaps were reduced: 3.50 €/100 kg carcass between pasture and European systems in 2005 and less than 1.5 € in 2013. China remains a special case with a very high production cost bound to the scarcity of inputs (feed, weaners), which is offset by a very high sale price of grown cattle (Figure 7).

Beef finishing returns and cost of production (results 2015). Source: GEB_ Institut de l’élevage from agri benchmark (www.agribenchmark.org).

The biggest beef and veal processing companies in the European Union are Bigard from France, VION from the Netherlands and ABP Food Group from Ireland (6.1%, 5.4%, and 4.2% of EU market share). The concentration of the beef and veal sector is low for the European Union, but much more important in some European countries such as Germany, France and the UK where it exceeds 50% of market share. Generally, retailers are increasingly the major drivers of change because they are taking control of the cutting and packaging of beef products and they are dictating characteristics of the animals they want to buy in terms of age, carcass weight and breeds. The meat sector generally has low economic margins [10].

Prospective

According to some studies, beef production is projected to slightly decline in Europe by around 7% from the 2010–12 average to a low 7.6 million tonnes in 2023 due, mainly to developments in the dairy herd, which represents around two thirds of beef production [26]. Because beef production will be lower than consumption, beef imports are supposed to increase, especially from Brazil, and to a lower extent from Uruguay and Argentina [26]. The consumption level in 2021 or in 2023 is projected to be stable [1, Table 1] or to slightly decline by 5.7% against the 2010–12 average. Tight supply is expected to keep prices firm around 400 euros/100 kg close to the record 2012 and 2013 levels (Figure 8). However, given the uncertainties relating to crop yields and the macroeconomic environment, prices may decline to around 300 or increase up to more than 450 euros/100 kg [26].

EVOLUTION OF CONSUMER EXPECTATIONS

Drivers of meat consumption

The habits of consumers are changing and meat has sometimes lost its central status in the family meal [27]. Indeed, consumers who have gradually less time to cook, and who are less and less present at home, often look for products that are quick and easy to prepare, which is generally not the case for fresh meat. Moreover, the traditional structure of the meal is tending to give way to more modern and more innovative forms of meal such as buffet or “dinner-aperitif”, etc. Fresh meat is not really adapted to these new modes of consumption, though processed meat together with burgers and minced beef that are easy to cook are benefitting from a market in constant growth. Furthermore, consumers are worried about the price (among the first factors of the purchase [28]). European consumers have also strong expectations in terms of eating quality, animal welfare, “traditional” extensive rearing methods, health-value of meat, environmental expectations, ecological friendly food production [2] as detailed in the Introduction. These aspects are not always compatible, the least expensive meat being associated with intensive production systems, which are often criticized by the media. These days, most consumers are urban and some incomprehension has emerged between meat producers and meat consumers, opening up a gap between them.

Consumer purchasing habits are also influenced by “news” and these effects can be of short or long effect. In Europe, two recent news stories exemplify this effect. The news in 2013 that some companies had been selling horse meat in place of beef, and that this product was now widespread across Europe due to extensive trade networks, caused the consumer to lose confidence in the supply of beef. Although horsemeat is not of itself harmful (though some drugs used in horses may be), the fact that unscrupulous dealers can substitute meat on a large scale raised ethical questions and suggested that controls were inadequate to protect food safety [8,29]. The economic consequences for the European beef industry are difficult to calculate [30].

In 2015, a paper was published by the International Agency for Research on Cancer [5], which proposed that red meat and processed meat products, increased the risk of certain types of cancer, and this news made headlines across the world. The Working Group classified consumption of processed meat as “carcinogenic to humans” and consumption of red meat as “probably carcinogenic to humans” based on the extent of the evidence for colorectal cancer and other cancers. A substantial reduction in the purchase of red meat and cured meat products during the following period was reported in the UK [e.g. 31,32].

Meat is, to some extent, a victim of its success. Formerly reserved for the favoured and most wealthy categories in society, meat is now consumed more and more from the bottom of the social ladder. Indeed, social behaviour is driven by both imitation and differentiation. The least favoured categories tend to imitate the wealthier ones by eating more meat. But more affluent groups try to differentiate from the poorest by eating less meat or different types of meat [33]. It is also the wealthier categories which are the most the sensitive to nutritional concerns and “noble” concepts of welfare and environment, for example. As food practices are conditioned by consumers’ social category and income level, these practices will continue to be powerful social markers [33].

In developed countries, there are approximately 5% of vegetarians (from 1% to 3% in France and in the USA to 12% in United Kingdom), with twice more vegetarians in the young population. Another trend, called “flexitarianism”, is also in development: it corresponds to an irregular and occasional reduction of meat consumption, meat being no longer the centre of every meal. This feeding behaviour is practiced for diverse reasons (support for causes such as animal welfare, environmental protection, concern about a more well-balanced diet, reduction of the size of the portions etc.). Nevertheless, these flexible consumers consume some meat during particular occasions (with friends, at the restaurant, etc.). Furthermore, 56% of French people declare to have reduced their meat consumption [34]. Whilst these trends are causing a reduction in beef consumption in developed countries, at the world level meat consumption is expected to increase by 70% from 2012 to 2050 [35].

The trend to consume less meat, in developed countries, explains why “meat substitutes” increased their market share during the last 10 years (http://www.grandviewresearch.com/industry-analysis/meat-substitutes-market). These meat substitutes are mainly products from tofu, but also from cereal proteins, mushrooms or textured vegetable proteins. Burgers with vegetable proteins represent an expanding market. It has been decades since the texturisation processes of vegetable proteins were studied. Nevertheless, it is only recently that the use of this type of product has spread in the food-processing industry. For example, the steak of the “Impossible Food” start-up (Silicon Valley) consists of wheat, coconut oil and potato. Besides its composition, this steak is “bloody” as a real steak thanks to the addition of “plant blood”, a protein extracted from legumes roots. More recently, the media have publicised the possibility of producing artificial meat by cell culture. The principle consists of the reproduction of undifferentiated and non-mature cells many times in succession. The “proof of concept” was demonstrated by a Dutch team, which produced the first “artificial burger” in its laboratories. The high price of this prototype (of the order of 280 k$ for one burger) makes impossible the idea of a marketing, at the current time. Artificial meat is based on the positive values conveyed by meat (good nutritional quality, symbol of strength, and pleasure to consume) while claiming a lack of disadvantages associated with meat production (no environmental degradation, no animal suffering, etc.) [reviewed by 13]. Baht et al [36] have proposed that the biofabrication of meat-like products in vitro has the potential to contribute to the challenge of feeding a growing population, while reducing environmental impact of a growing beef population, but that there are some technological barriers yet to overcome. However, this innovation is subject to numerous limits, especially in the following fields: societal and technological, economic, environmental, ethical … [reviewed by 13]. Other long-term initiatives have also been proposed, some unlikely to be socially acceptable: for example, a Japanese scientist cleanses proteins from the sewage sludge of the city of Tokyo (rich in human excrements) to make them edible. These initiatives relied on “anti-meat” arguments: the lack of animal welfare perceived in certain types of production, the necessity of respecting animals, the decrease in environmental degradation, the need to feed 9 billion human beings in 2050, the suggestions that meat is not be good for health, etc. These arguments have been challenged by several authors [4,37,38] At the moment, it appears that the main limiting factors for their development are i) their production cost and thus their selling price, ii) their environmental footprint, and iii) their gustative and cultural acceptability by the consumers. These factors may change as these types of products are further developed. The value of meat to customers may ultimately be affected by the presence of these alternative products [39].

Evolution of consumer concerns

Despite the previous discussions, it remains important not to forget that eating meat is a pleasure for a large majority of the European population. For example, meat has its place in the “French gastronomic meal” registered by UNESCO. Indeed, the “French gastronomic meal” was registered in 2010 on the Representative List of the Intangible Cultural Heritage of Humanity (https://ich.unesco.org/en/RL/gastronomic-meal-of-the-french-00437). During this festive meal, the dinner guests practice “the art of eating well and drinking well”. The gastronomic meal emphasizes i) the fact of being together, ii) the pleasure of the taste, and iii) the harmony between human beings and nature’s production. The gastronomic meal has to respect a defined plan: an entree or starter, a fish and/or a meat with vegetables, a cheese and a dessert.

The role of beef in the European diet has been challenged by evidence that too much red meat can be harmful. The World Health Organisation (WHO) have issued guidance that people should limit their intake of fat to 30% energy intake, while minimising saturated fats [40], in order to protect against cardiovascular disease and stroke. Ruminant meat and dairy products have been cited as a primary source of these saturated fats [5], though there is now some question whether saturated fats are always harmful (http://www.ateneo.edu/news/features/warning-saturated-fat-defective-experiments-defective-guidelines). Recent evidence that red meats can increase risk of certain cancers [5] is concerning to many consumers and WHO recommend that individuals concerned about cancer should limit their consumption of processed meat and red meat “until updated guidelines related specifically to cancer have been developed” [41]. The role of red meat as a supply of essential nutrients is acknowledged [41,42], but advice is unclear on whether red meat should be consumed and in what quantity [41]. The WHO advice states: “Eating meat has known health benefits. Many national health recommendations advise people to limit intake of processed meat and red meat, which are linked to increased risks of death from heart disease, diabetes, and other illnesses”. “The risk increases with the amount of meat consumed, but the data available for evaluation did not permit a conclusion about whether a safe level exists”.

Meat makes an important nutritional contribution to bio logical balance of the human body. Beef contains 26% to 31% of proteins, while its average lipid content is low (6% in average, with lean pieces: 2% to 4%, and fatter ones up to 11%; [43]). Beef also brings essential amino-acids, vitamins (especially B12 vitamins), and trace elements (such as Zinc, Copper, and Iron). In addition, there is evidence that many of the peptides derived from beef are biologically active and make a positive contribution to antihyperthensive, andioxidant, anticancer, antimicrobial, activities [44,45] and interest has been shown in potential uses of bioactive molecules [46]. So, beef, through its content of proteins and minerals, can play an important role in the food balance [47]. Needs are different according to age, physiological situations (such as pregnancy or activity level). For populations and groups which do not eat meat, careful food combining is needed to ensure that there is sufficient intake of iron and other micronutrients to meet human nutritional needs [48]. So consumers are facing a difficult dilemma: what is the right amount of red meat to consume for the health of their families and themselves?

European consumers have many choices when purchasing food for their table. Given the high price of beef, they expect that their purchase will provide both pleasure and nutritive value. Thus, the challenge for both producers and suppliers is to be able to produce beef that meets consumer expectations at the right price. In Europe, beef is valued by carcass grading based on conformation and fat class. This system was developed as a basis for trade (reviewed by [18]). However, this grading does not guarantee sensory or nutritional quality. Evidence based on data from five European countries showed that 19% grilled sirloin, 25% grilled rump and 53% roast topside was judged to be “unsatisfactory” by consumers [49]. This issue is nowadays the subject of extensive research across many countries and innovative approaches have been developed to predict meat sensory quality (reviewed by [15, 50]), and other intrinsic qualities of beef, e.g., for example nutritional qualities (reviewed by [51]).

In this context, another question is raised: the value of meat products to the customer. This concept relates to the amount that a customer is ready to pay to buy a product. If the customer value (that the consumer attributes to the product) is higher than its real price, the consumer will buy the product. Otherwise, (when the customer value is lower than the effective price) the consumer gives up the purchase [52,53]. This point is important, since no clear relationship has been established between the sale price of a product and its sensory quality, especially its tenderness in the specific case of beef meat [54].

The consumer has generally only a few minutes to make a purchase decision. Therefore, the initial impression of the product to the consumer is very important and the integration of intrinsic and extrinsic quality characteristics has to be rapid. For this reason, the characterization of meat products is highly dependent on marketing. As good meat hygiene is generally considered to be a prerequisite, consumer choice is based on brand, appearance, marketing image and/or simplicity of use. Thus, to maximise consumer purchases, it is necessary to seduce the consumer. This involves developing real marketing and commercial steps and these aspects are nowadays insufficiently developed in meat sector [55]. This is especially important as, when there is no convergence between the characteristics desired by the consumer at the time of the purchase and those perceived at the time of use, the weight of the information given to the consumer at the time of sale becomes very important (even often prevailing). Furthermore, it is necessary to take into account psychological, marketing and sensorial factors, as these parameters influence the consumer in terms of preference, behaviour and perception toward meat and meat-products [reviewed by 28].

Over time, consumers’ expectations have evolved and di versified. In the past, nutritional adequacy, safety and, of course, price would have been the prime concerns. However, now consumer aspirations also include numerous intrinsic and extrinsic qualities. These include nutritional risks as well as benefits, eating quality as well as carbon impact, animal welfare and sustainable production. All these expectations, sometimes mutually contradictory, must nevertheless be jointly satisfied (reviewed by [15]): these are the current challenges that the meat sector has to address.

Towards a better prediction of eating quality?

Over time, in order to better meet consumers’ expectations, especially in terms of perceived eating quality, many different strategies have been developed. Most of them have been based on specifications for beef producers. In other words, if producers follow some specific rules of production, specific labels or brands will buy their products. Some well-known official brands certify either origin (more or less associated with a better eating quality) or true eating quality. The labels of origin in Europe were initially motivated by three major reasons. One was the desire to fight against usurpation of famous names associated with a specific region (such as the French wine, “Champagne”). Another goal was the need to provide to consumers products of high and/or typical quality produced in an animal-friendly way and with respect for the environment. The last goal was to maintain and develop sustainable agriculture and to maintain the presence of producers and farmers in rural territories famous for their agricultural products. Therefore, three EU schemes known as protected designation of origin (PDO), protected geographical indication (PGI), and traditional speciality guaranteed (TSG) promote and protect names of quality agricultural products and foodstuffs. PDO covers agricultural products and foodstuffs which are produced, processed and prepared in a given geographical area using recognized know-how. PGI covers agricultural products and foodstuffs closely linked to the geographical area. At least one of the stages of production, processing or preparation must take place in the area. TSG is different since it highlights the traditional character, either in the composition or means of production. In addition to these labels, the indication “Organic Farming” certifies the mode of production and processing does respect natural balances and animal welfare as defined in a highly stringent set of specifications. The French agricultural quality label called “Label Rouge” certifies that the product quality higher is than that of a similar product of the standard type because it has been produced according to specific rules. Awareness of these labels varies across European countries: it is generally higher in Southern countries of Europe (reviewed by [15]). Quality labels have also been developed in other countries, such as “Red Tractor” in the UK (https://www.redtractor.org.uk/choose-site).

Several international Workshops have been held to dis cussed the future of the beef industry, one in Clermont-Ferrand (INRA-Theix, France) on 9–10 September 2009 [56], one in Paris on 20–21 August 2015 [57] and two in Milan [9,49]. A first conclusion was that, in the area of product quality, the existing knowledge is not fully applied by industry actors for different reasons, which may be economic, social or political, linked, at least in part, to the organization of the beef industry itself. As a consequence, there is a need to develop methods to monitor or predict eating quality in order to reduce its inconsistency. In fact, beef palatability has been the subject of active research for many decades. Research has been conducted in animal genetics and husbandry, slaughtering procedures, meat ageing, and processes. However, the consumer has rarely been at the centre of these research concerns. This has induced some bias. For instance, beef producers in Europe are currently paid according to carcass weight and characteristics (conformation, fatness) which are of interest for the meat processor (because linked to yield). However, it was shown that the eating quality score of beef does not depend on these characteristics [58]. Consequently, European producers are currently motivated to produce heavy and lean carcasses, which give more meat per animal and hence allow them to earn more money. They should be financially encouraged to change their practices to produce better beef.

The global beef industry has yet to agree on one method for ensuring that eating quality meets consumer expectations. The meat industry and researchers have investigated a range of methods for predicting and managing eating quality and these have been reviewed recently [50,59]. A wide range of new technologies have been evaluated for the prediction of eating quality [60] but none have yet achieved this consistently and grading methods still deliver the most reliable prediction. One way to deliver consistent beef eating quality in Europe would be the development for Europe of a prediction model similar to the Meat Standards Australia (MSA) System [15]. Unlike previous strategies (PDO, PGI, label Rouge, etc), the MSA system is focused on the eating quality response of untrained consumers, which form the population who purchase meat. This innovative grading scheme predicts beef quality for each individual muscle×specific cooking method combination, depending how long beef is aged and using information on the corresponding animals and post-slaughter processing factors. These factors include the percentage of tropical breed content, steroidal growth promotion implants, sex, overall growth rate, ossification index, ultimate pH, carcass fatness, meat colour, carcass weight, carcass hang method, etc.. Each cut receives a meat quality score (MQ4) between 0 and 100, based on a prediction and combination of 4 traits assessed by consumers: tenderness, juiciness, flavour and overall liking. The MSA system has proved to be effective in predicting beef palatability not only in Australia but also in many other countries in North America, Asia, South Africa and also in Europe as demonstrated by the work conducted within the EU-funded ProSafeBeef project, together with national projects in a number of countries [15,61–67]. The current usage of MSA in Australia is high and the total number of carcasses graded is continuously increasing, reaching about 38% of total Australian slaughter [68]. More recent studies have estimated the financial benefits through the supply chain to the retailer, wholesaler and the producer which deliver on average $AUS 0.24 per kg carcass weight. In other words, even if the MSA research initially targeted consumers, it has also been profitable for all actors of the supply chain [68]. This is a very good example of a “win-win strategy”.

Towards a better assessment of “goods and services” derived from livestock farming?

In addition to eating quality, consumers are more and more concerned by other quality aspects such as the nutritional value of beef, livestock production practices and the environmental and land management impacts of beef production. This idea directly questions livestock farming systems. While the importance of livestock for humanity has been acknowledged for centuries, there is no methodology to quantify it, and this is especially important in the current human societies where urbanization has induced a decreased awareness of the role of livestock production. A recent study [4] has first listed goods and services derived from livestock, goods and services being understood as tangible outcomes and benefits to society. They were grouped into environmental, economic, rural vitality and cultural goods and services based on previous studies such as Lynch et al [69].

In a second step, the collective group of the 13 authors of the study of Ryschawy et al [4] has listed 33 goods and services and has defined relevant indicators of them.

In a third step, following statistical analysis, a typology of goods and services was proposed (Figure 9). It was observed that “ruminant meat production” was positively correlated with almost all goods and services of the two categories “provisioning” and “rural vitality”, and with “maintaining temporary grasslands” and “heritage landscapes”, with only one significant negative correlation (with “agrotourism”).

Finally, four “goods and services bundles” were defined: type 1 called “provisioning and vitality” with high levels of food provisioning and rural vitality, but inversely related to environmental good and services [4]. A typical example of this bundle is in Brittany, a French region in which intensive livestock farming dominates. Type 2 has been defined as multifunctional bundle, with contribution of diverse goods and services (the four groups of goods and services being equally represented). A typical example of this bundle is “Massif Central”, a central region of France where extensive ruminant productions on pastures dominate. Type 3 bundle was called “cultural” bundle. It is associated with cultural and some environmental goods and services. It is observed in high mountainous and unfavourable pedo-climatic regions such as in the Alps. Type 4 bundle “depleted” bundle is characterized by low levels of all goods and services, it corresponds to regions where livestock farming has declined a lot over the last decades and where such farming is probably no longer viable.

This type of reasoning can be extrapolated at the European level or even at the World level since many different types of farm exist. They can be classified as shown below (http://thebritishgeographer.weebly.com/spatial-patterns-of-food.html), although, in reality farms are often a combination of different types:

Commercial Farming - the growing of crops/rearing of livestock to make a profit

Subsistence Farming - where there is just sufficient food produced to provide for the farmer’s own family

Arable Farming - involves the growing of crops

Pastoral Farming - involves the rearing of livestock

Mixed Farming - involves a combination of arable and pastoral farming

Intensive Farming - where the farm size is small in comparison with the large amount of labour, and inputs of capital, fertilisers etc. which are required”.

Extensive Farming - where the size of a farm is very large in comparison to the inputs of money, labour etc. needed

Agribusiness - involves the large corporate organisation of farming- often farms are run for profit maximisation and economy of scale”.

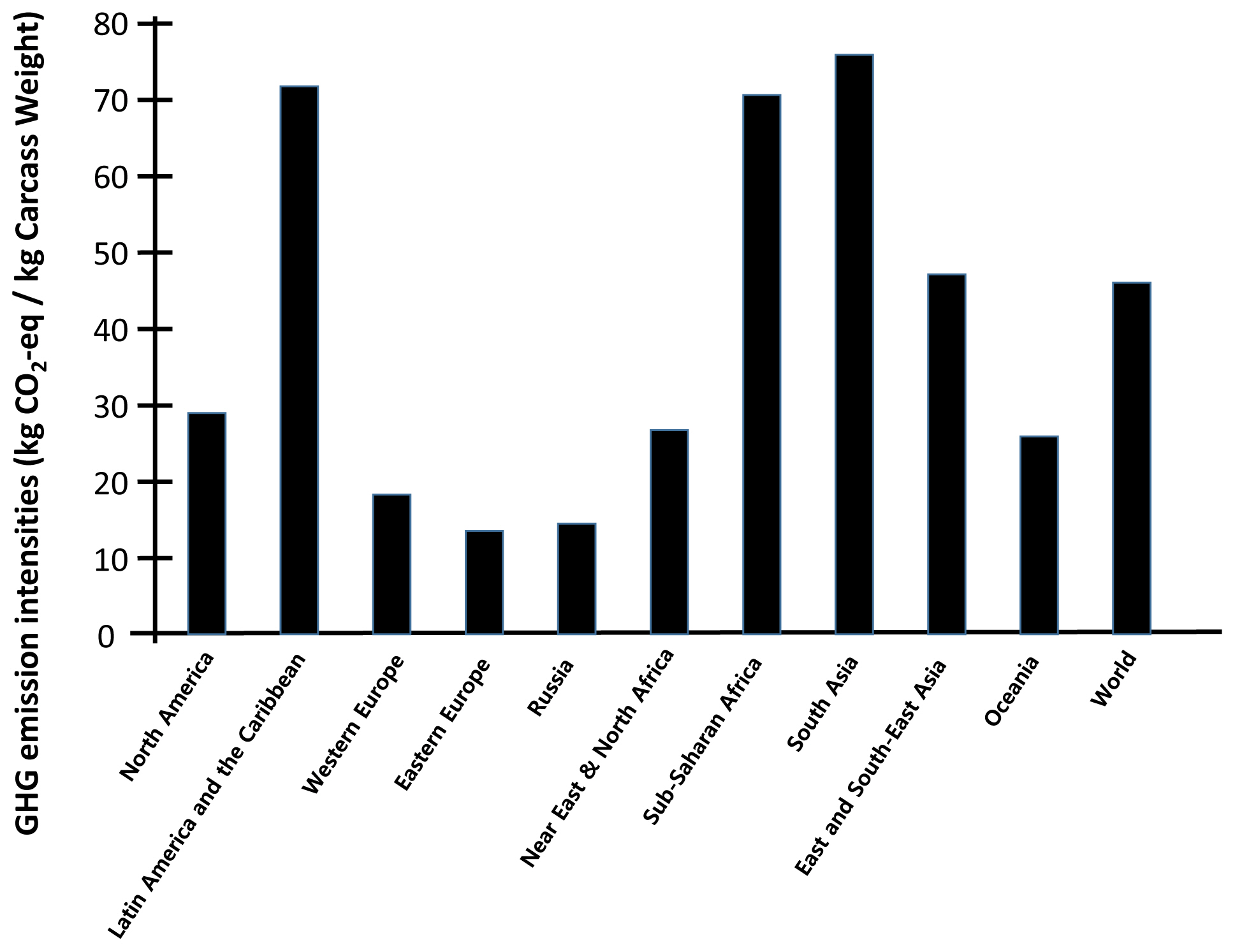

We suggest that the methodology applied to France by Rys chawy et al [4] is extrapolated to better assess livestock farming systems and the different production types (meat, milk, etc). Some partial attempts have already been reported [70]. For instance, in the case of beef production, Gerber et al [3] have found a low contribution of beef production in Europe to the total world GHG emissions (Figure 10). However, within Europe, there is a factor of 2.6-ratio difference in GHG emission per kg of beef between countries [71].

Future scenarios

A recent prospective paper on the evolution of the beef sector [72] proposed four groups of essential determinants: i) evolution of European consumption, ii) climate change, iii) introduction of sector environmental policies and 4) sector organization. As the meat sector has to tailor its business as closely as possible to “meat consumption”, this determinant appears to have a central position. Consumption will be impacted by the other determinants. Cerles et al [72] observed from the past a long-term downward trend in individual consumption of beef. This trend may be increased, maintained or underestimated in future extrapolations, which would lead to hypotheses that consumption will decrease by, respectively, −5%, −30%, or −60% between 2015 and 2050 [72].

Cerles et al [72] also developed different regional scenarios, which may be extrapolated to European level: i) The first one is based on the production of an excellent meat, in a context of European consumption strong reduction. In that scenario, the consumer rejects intensive production methods. ii) The second scenario is based on a liberalization of markets. In that context, a direct competition between the regions that produce meat will appear. Every region will have to adapt itself by saving and by reducing drastically its production costs. iii) The agro-ecological scenario gives an answer to the societal expectations expressed in favour of ecosystem friendly products. The “conventional” agriculture will become a “sustainable” agriculture. The use of agro-ecological practices [73] becomes a trend whereas the organic farming becomes widespread. The systems of production are economically, socially and technically optimized. The aim is to promote diversities, complementarities and mixing between systems, species, etc., in order be the most efficient possible and to answer positively to demanding environmental standards. iv) The “partnership” scenario is based on fair and constructive partnership, also recognized between producers, transformers and distributors. v) The “geopolitical” scenario is based on a strong European policy in the regulation and the development of proximity export markets, in particular with the countries of North Africa and the Middle-East. Beef and sheep meat participate in the market products that are trans-Mediterranean guaranteed.

Other authors [74] emphasized the needs of strategies to achieve sustainable diets lower in greenhouse gas emissions: they include setting up a carbon tax or a carbon labelling, to reduce food loss and waste and/or to adopt new technologies at the farm-level. The major question underlying these strategies is how individual food choices will have the potential to influence healthiness of human diets and the environment. These authors concluded that a reduction in meat consumption does not necessarily induce a reduction in overall emissions. It may be the opposite (i.e. an increase in emissions) depending on the foods used to replace meat. The balance between supply and demand of food is a key step in reducing emissions, as well as focusing on human health for policies and strategies [74]. This conclusion was confirmed by other authors who claimed that “diet change strategies should focus on the level of the whole diet” rather than on one compound of the diet, such as beef [75]. Indeed, it has been calculated that about 21 g of protein from animal source food (which includes beef) can be produced for each person per day with no competition for land between feed and food production, the recommended intake of total protein being about 60 g/person per day [38].

Whatever the future, while additional research is in prog ress to combine animal performance, nutritional value and sensory quality of meat in a global index of quality for consumers [76], environmental impact of beef production has to be considered in this index as well. It will be also be necessary to evaluate the future development of farming systems (in terms of food resources, animals characteristics, environmental impact of production, etc) and its impact on meat quality, on sector efficiency, and finally on the economy and the sociology of production and consumption.

CONCLUSION

A big challenge for the European beef industry is the regular decline of beef consumption per capita. The purchasing power of consumers is a key determinant of the level of meat consumption per capita. This is particularly true in the beef sector because beef prices at the consumer level are generally higher than those for other types of meat. In addition, gaining market shares outside Europe is also important for the future of the European beef industry. But the European beef market is weakened by the fact that the world market is dominated by four major bovine meat exporters that are highly cost-competitive (Australia, India, Brazil, and the United States).

From an economic point of view, one major problem and challenge for the beef sector in Europe is its heterogeneity across countries, not only in terms of beef consumption per capita, but also in terms of cattle distribution, farm size, price, cost, economic profitability, incomes of farmers, livestock practices, etc., especially between north-western, north-eastern, south-eastern and south-western corners of Europe. Cattle fattening is a major farm activity in Ireland, Scotland, northern Spain, central France and Sweden. However, most of the fattening farms are located in Ireland and North-West Spain (which is logical) but also in Poland and in or around the Alps. In some specific regions, the agricultural sector depends a lot on beef production. The least opportunities are for some Eastern countries or arid regions around the Mediterranean Sea. The smallest specialized farms have less capacity for investment and innovation and are, therefore, more vulnerable. Carcass weight is currently one of the main drivers of income levels. The huge differences in labour incomes associated with beef production is also an important challenge for the viability of fattening farms in some regions.

From a social point of view, high stocking densities became a challenge due to environmental issues. Societal discussion about environmental issues due to concentration of animals (i.e. high stocking densities) is increasing especially in the Benelux, North and South of the Alps and Northwestern of France. Societal protests against slaughtering practices is also increasing. National regulations are often implemented to address such concerns but they may impair the economic competiveness of the beef supply chain.

On a long term-basis, as in other developed countries, the European meat sector is at a crossroads, due to increasing consumers’ expectations. In addition to traditional concerns for price, quality and nutritional value, societal questions appear to be more and more important. This raises new research questions in the fields of the human and social sciences, such as the impact on degradation of the environment and the global warming. It is impossible to dissociate meat from the livestock from which it arises. By combining expert opinions and literature reviews on the subject, it has been established that livestock farming systems provide consequent goods and services, in particular in terms of production of food (especially proteins), of environmental quality, territorial vitality but also of cultural identity. Recent reviews listed livestock assets while fighting the excessive simplifications, which lead to a focus that is too narrow. Indeed, nowadays in the media, the services provided by livestock and their positive effects are less considered than its negative effects, thereby negatively influencing consumers’ opinions. For example, the exploitation and valorisation of certain feeds, in particular grass, by ruminants is generally forgotten. However, human beings cannot gain financial value from meadows without herbivores.

In Europe, the pursuit of technical evolutions will be nec essary to produce beef in the right quantity and quality to satisfy consumers. Thus, the search for quality prediction makes perfect sense and the development of a prediction model similar to the Meat Standards System is a good example. Such developments are also likely to encompass systems such as MSA and instrumental measures as the technology develops. On the other hand, the relationship between humans and meat as a food continues to evolve. In some sectors of society, this may include an increase in “eating well” and gastronomy, and a trend in favour of locally produced meat, with such meat being supposed of better quality, and more protective of the environment. It is thus likely that the consumption of locally produced food (close to the place of residence) or stemming from organic farming or from agro-ecological farming will continue to develop. It is not very probable that the “flexitarianism” will quickly go out of fashion, as this movement is “in sync” with the questionings of our society (in particular when concerning young people that will be the consumers of tomorrow). However, with economic pressures on family incomes for many people, the price of beef and its value for money is likely to continue to be important. At the same time, the technical progress (cloning of animals, artificial meat production) opens new ways of evolution, which may be in contradiction with previous food production methods.

Taking into account these economic, environmental and societal issues, and the inherently high cost of European farming methods compared to ranching in less populated parts of the world, producing high-quality and premium beef, with high extrinsic quality traits (i.e. with non-food benefits for the society) is probably the most promising direction for the future of the beef industry in Europe. This is an opinion shared by stakeholders, some of them saying that grading systems should be more consumer focused. Thus, one key area for the European beef industry to address is high value adding and integration of consumer concerns. Most human beings remain fundamentally omnivorous and a varied diet, without quantitative or qualitative excess, is recommended by the nutritionists. The European meat sector will need to constantly adapt itself in order to satisfy evolving consumer expectations. Thus, the European beef industry’s future is to answer the challenge to its durability through by protecting food safety, ensuring nutritional and gustative quality, protecting the environment and animal welfare, while maintaining a balanced land use and landscape quality.

Notes

CONFLICT OF INTEREST

We certify that there is no conflict of interest with any financial organization regarding the material discussed in the manuscript.